Besides loving education, summers off (for those of you not teaching summer school) above-average income (average Canadian employment income according to StatsCan age 45-54 is $64,800; age 35-44 was $59,600) plus benefits, teachers will receive a great pension.

The Ontario Teachers’ Pension Plan provides a pension income example: If you earn $85,000 in your five highest salary years and have 30 years of credit, your basic annual pension would be 2% × 30 × $85,000 = $51,000.

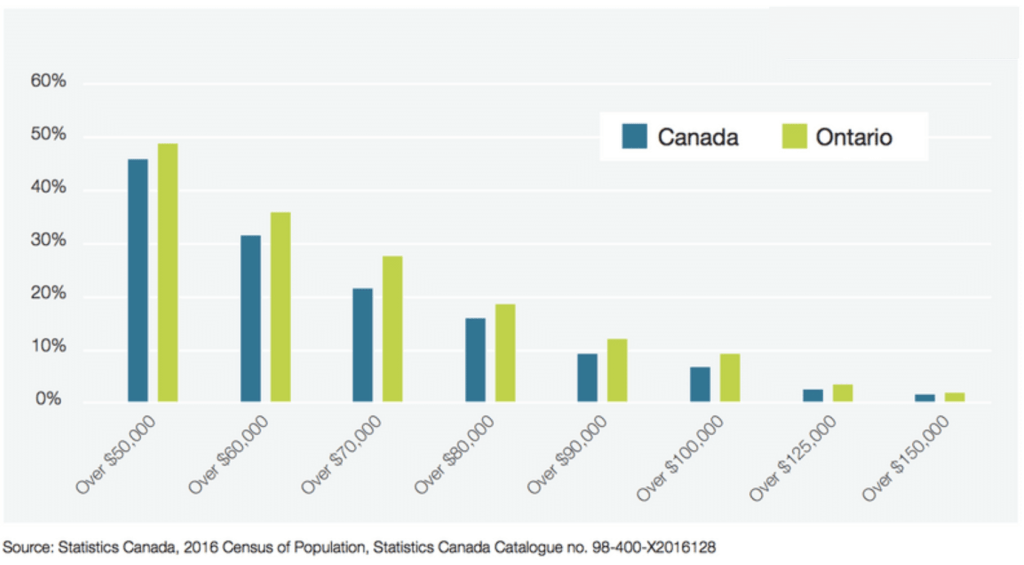

According to StatsCan, a retired couple had annual expenses between $40,800 to $48,600. Approximately 50% of retired couples have a combined total after-tax income greater than $50,000.

Couple: Cumulative after-tax income

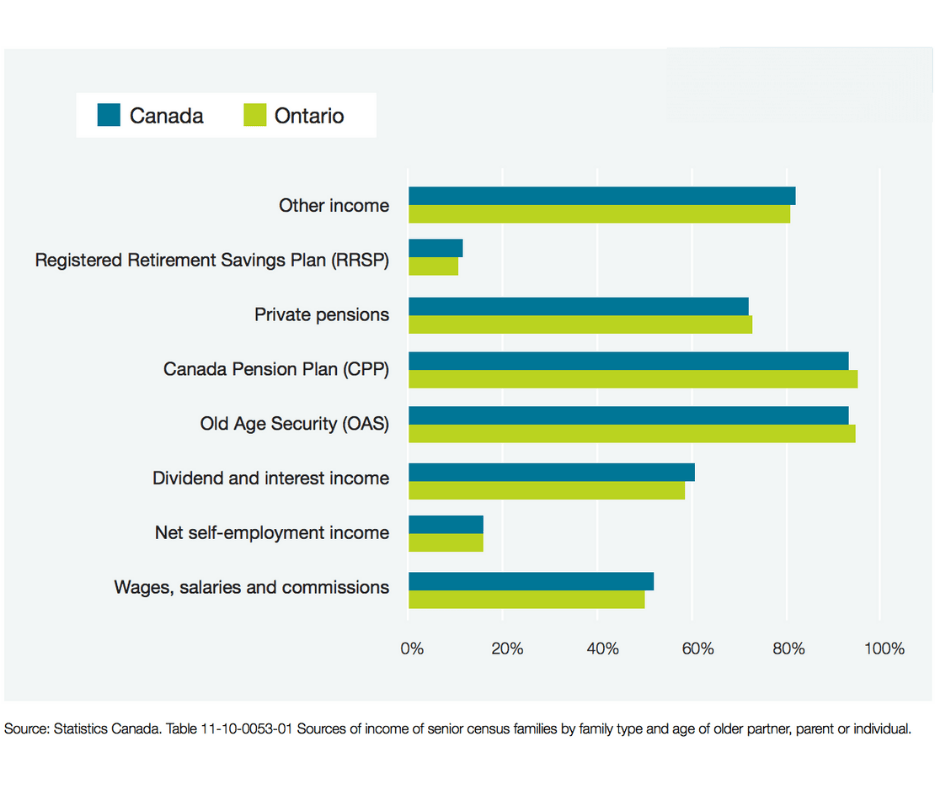

Sources of Income

When teachers marry teachers

When teachers marry another teacher and work as a teacher until they retire, their combined retirement income will provide income well above their living expenses (assuming they don’t try to live like the Kardasians). They will have roughly $30,000 of additional after-tax disposable income to spend any way they want. The #1 concern people have about retirement is: Will I have enough money to retire? When a teacher marries a teacher, they will not have that concern.

When you pray for rain you have to deal with the mud

Two married teachers really need a financial advisor because they already have their retirement income goal solved. The issue is where do you invest the excess cash you have throughout your retirement years? An RRSP will only create a larger taxable income for you. You’re also going to lose about 35% to taxes at the last death of the couple. What you need is a pool of money that will provide a non-taxable income stream at retirement (if you need it).

The #1 Wealth Building Strategy for Teachers

What if I told you, that you could invest into something that is boring, returned 5-6% per year with no tax, low risk, and if you died would pay your spouse more than 10x what you invested tax-free! How much money would you invest? Sounds too good to be true although this is the one exception that breaks the rule.

It’s Participating Life insurance. There are many advisors who will suggest using Universal life insurance however this should be avoided if using this strategy for wealth building. It may be the only type of permanent insurance the advisor sells, so ask questions.

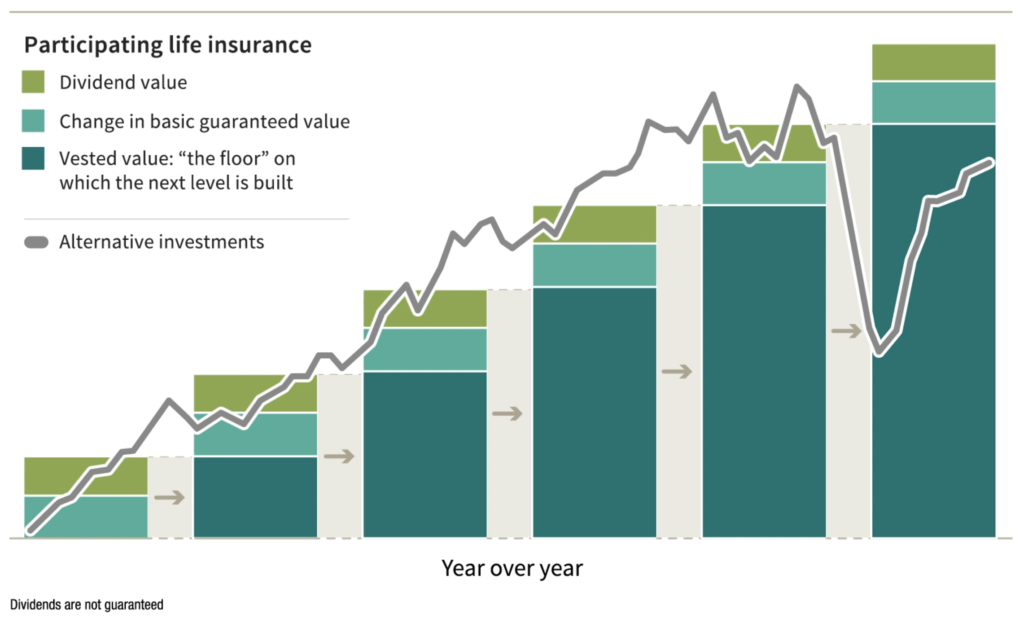

The advantage of participating life insurance is the accumulated cash value in your policy. When the annual dividend is deposited to your policy, it is reinvested into the fund producing compound returns, and because of the nature of how insurance cash values are invested your balance never decreases unlike investing in an RRSP. The illustration below compares the year over a year difference between accumulating cash values vs. the stock market. Note the far right column with a severe market decline (due to Corona Virus). The growth in the insurance cash value was unaffected and continued to grow.

In this strategy, you would deposit money to the insurance policy the same way you would if you were investing in an RRSP. The excess cash above the actual cost of insurance is invested in a fund managed by the insurance company (the fund is actually huge, about $41 billion). Because the money is used to pay death claims & dividends, the investment allocation has to be conservative. You’ll find about 20% of the fund is invested in the stock market and the rest are bonds, mortgages & private placement. The fund is largely unaffected by severe downturns in the stock market.

Not all investments are equal

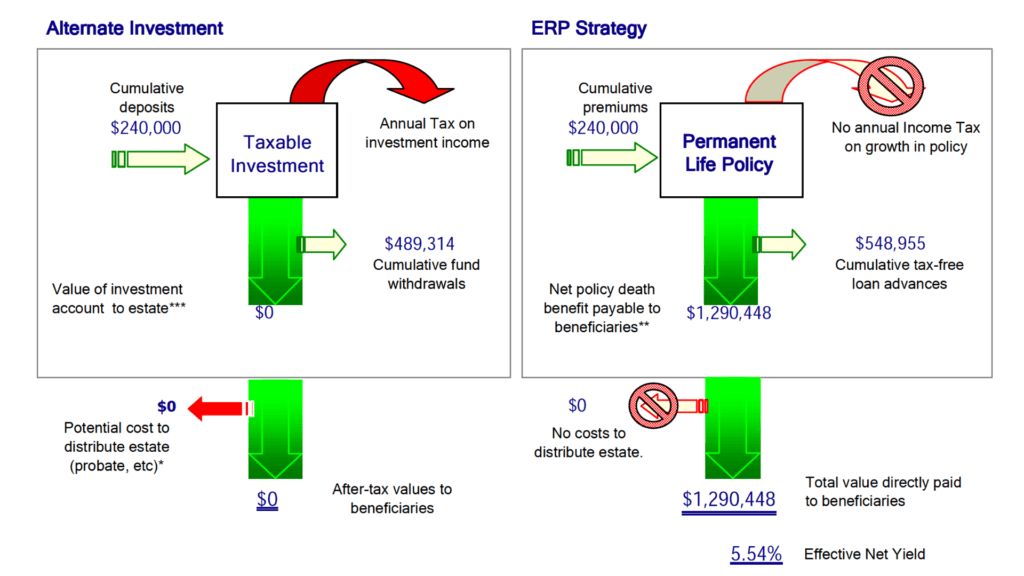

The illustration above compares a non-registered investment vs the participating life insurance. In this example on the left, we are depositing $1,000 per month for 20 years. In the mutual fund, $240,000 is invested and grows at 7% but is taxed each year. Annual taxation on the fund is a drain upon the longevity of the use of funds. A total of $489,314 is withdrawn over retirement. The owner passes away and there is No money left to pass to his/her heirs.

In the insurance example on the right, the same amount of money is invested, $1,000 per month for 20 years for a total of $240,000. There is no tax on the growth of the cash value which is one of the main advantages of participating life insurance. Over the course of retirement, the owner withdraws $548,955 ($59,641 more than the mutual fund) and the owner passes away at the same age as the mutual fund example. At his/her passing, $1,290,448 goes to his/her beneficiaries tax-free!

Clearly, the life insurance investment a superior wealth building solution as compared to an RRSP.

Additional advantages

Two teachers with pension income and RRSPs accounts will likely experience a claw-back of their government retirement income whereas, the income received from the life insurance is tax-free and will not affect their government retirement income.

It may seem like an oxymoron to talk about retirement and post-retirement careers in the same article. But it’s also not uncommon for people to retire from one career field only to transition into another.

Even apart from retirement, a study found that 17% of teachers leave the field within the first five years of entering. We can presume that a higher percentage leave sometime after the first five years.

The point is, there may be a career change in your future. And that change may happen once you retire. At that point, you might be done with teaching, but you might want to try your hand at something different.

Why You Might Want to Retire Only from Teaching

There are all kinds of reasons why you might only want to retire from teaching. Here are some I was able to come up with, but I’ll bet you can come up with a few more.

Greater financial independence. If you have a pension and a well-funded retirement savings plan, you may feel empowered to try a different career field. After all, you won’t have the same financial dependence on your career that you have right now, so you’ll be free to try your hand at anything that you want.

You’re retired, but you’re not “finished“. This is not an unusual situation at all. Many people simply want to retire from the career they’ve been working at all their lives. But it’s not to retire to the beach and play golf. You may feel that you have a lot to give in a similar or even totally unrelated field.

You may want to work at something. Some people can’t wait to retire to a life of blessed nothingness. But others enjoy work, and can’t imagine living life without it. You may want to give up the rigors of teaching, but continue to work at something that’s equally satisfying, but less stressful.

You may find your passion late in life. Or you may have been aware of your passion all along, but you have been afraid to pursue it for fear of financial difficulties. But once you reach the point where your children are grown and the heavier obligations of life are behind you, you may want to finally pursue your passion, at least on a part-time basis. Once again, having a pension and retirement plan will make the jump easier.

What kind of post-retirement careers might you want to take a shot at?

1. Professional Speaking

This field is a natural for teachers. After all, as a teacher, you regularly stand up before a group and give a speech. In fact, it’s what you do on most days during your career. You’re probably more accomplished at it – and more confident with it – than the average person.

This isn’t a small point either. Most people rank public speaking as one of their greatest fears, right up there with the fear of venomous snakes. An article in Psychology Today provides clarity on why people fear public speaking.

The reason I point this out is because, as a teacher, you need to understand that what is a basic skill for you in your career is terrifying to other people. Your ability to speak before groups is unique and has market value.

You can turn your public speaking skills into professional speaking, by entering a career or business where you will be presenting to groups. That could involve doing presentations on important issues, providing group training, conducting seminars, or even doing group sales pitches.

If you can stand to do an all-day presentation to a room full of kids, spending an hour or two in front of a group of adults should be a piece of cake!

2. Anything Involving Research

Research is another part of the job for teachers. But like public speaking, it isn’t something that everyone is comfortable with. As a teacher, you’re familiar with the methodology of research, as well as with determining what’s relevant, and learning how to package and present it.

Since research is necessary in so many areas, there’s almost no limit to how and where you can apply it as a post-retirement career.

There’s medical research, legal research, scientific research, technical research, social research, political research and marketing research – just to name a few.

Research would probably be one of those career transitions that will be very short for a retired teacher. Since you already know the basics of research, it would just be a matter of learning to apply those skills to the discipline at hand. And if you’ve been teaching multiple subjects during your career, transitioning from one discipline to another shouldn’t be all that hard either.

3. Writing and Editing

As a teacher, you learned how to write before you even got out of college. And since you spent a career correcting papers, you’re also thoroughly familiar with editing. Even if you’ve never done writing or editing professionally, you already have the basic skills required to do either. That will give you a leg up in entering either as a post-retirement career.

Technical writing is also an extremely broad field. For example, you could write articles, marketing pieces and research papers for law firms, medical practices, marketing firms, small, medium and large companies, municipalities and nonprofit organizations.

You can also ghostwrite. There are many business people and executives who need to publish content on a regular basis, but don’t have time. You can take the writing skills you learned as a teacher, and use them to become the written voice for other people.

You can also do editing work in any of the above capacities. There are many people who write in today’s world, particularly because of the Internet. But not everyone knows basic grammar or sentence structure, or knows how to organize their work in a cohesive manner. You can.

With both writing and editing, you have the ability to work as an employee or as a contractor, or even to run your own business providing the services. There’s a lot of flexibility in this career field. You could even find yourself writing a book or an e-book for substantial compensation. Writing or editing can be a perfect work-at-home situation, too.

4. Corporate or Government Trainer

If you’ve been teaching kids for years, you’ll be a natural in training adults. The big advantage here is that adults who are undergoing career training are usually more attentive than a room full of highly distractible kids. The adults want to learn, because they need the information and knowledge for their jobs.

As a teacher, you’re well qualified to make this transition. Once again, you’re very familiar with standing up in front of a group and making a presentation. You’re also comfortable creating and using visual aid presentations.

The potential list of income-generating opportunities here is also limitless. Companies need trainers, whether on an occasional basis or continuously. We live in a world where technology, regulations, and consumer preferences change regularly. All that requires ongoing training. In most cases, you wouldn’t have to prepare the training material but just present it.

Training opportunities can also exist in governments. This is particularly true since government employees often need specific training to deal with the many changes in laws and regulations, and how to carry them out in their jobs.

5. Tutoring

Every post-retirement career idea that we’ve discussed so far is a natural fit for teachers. But tutoring is a virtual glove fit. That’s because you’re taking your skills as a teacher, and moving them from a group situation to an individual one. It’s a potentially lucrative field, too.

Tutors working with high school and college students can easily earn between $30 and $50 an hour. The better pay tends to be in the tougher subjects, like math and science, or prepping for high-stakes exams. As a teacher, you’ll know exactly what to do in each case.

A big advantage of tutoring is flexibility. Though there are certain jobs for tutors, most work independently. They develop their own client bases, either by advertising in local publications, or offering their services through schools, colleges, houses of worship, and government agencies.

Apart from school students, there are all sorts of opportunities for tutoring at the adult level. English as a second language (ESOL) has become a very popular study program for recent immigrants. You could also help to prepare people for the general equivalency diploma program (GED).

If your teaching background does include math or science, you’ll have a big, high-paying client base. But just about any subject you can think of has plenty of room for tutors.

6. Career Coaching

This is a more limited field since you will most likely be coaching students on how to prepare for careers in teaching. It’s not as common as career coaching and other fields since teaching has a specific career path.

But a potential market are people who are looking to transition into teaching from other fields, or even new teachers who are looking for coaching to advance their careers.

7. Consulting

This is a much more open-ended career field than the others, only because it’s typically less well defined. For teachers, there may be a limited number of specializations, but those could be lucrative.

One obvious consulting area is in the profession itself. You may be able to work as a consultant for underperforming school districts, or those that need help in a very specific area. As a career teacher, you may be able to offer hands-on skills, as well as the kind of perspective that only a well experienced outsider can provide.

Another area is working with companies who sell to school districts or the teaching profession. With your lifelong experience in education, your consulting skills may be a valuable addition to a business that is looking to either enter that field, or expand the business they already have.

There may also be government agencies or nonprofits who are working with children, or plan to do so soon. As a teacher, having spent a lifetime working with kids, you may be uniquely qualified to come on board as a consultant in some capacity.

Consulting is mostly about identifying niches, and then tailoring your skills to fill the need.

8. Paralegal

One of the factors that makes former teachers naturals paralegals is the discipline that you acquire with technical material. Paralegal work involves a great deal of research, which teachers are fully trained in. Your ability to access information sources, and organize technical information in a readily usable form will be a huge asset.

Since it involves the law, paralegal work requires a great deal of accuracy. But again, your training as a teacher has made this a part of your career already. You already understand the importance of being complete and readily presentable. And as a professional yourself, you should be well able to work with other professionals, such as lawyers in the parallel professionals that they deal with.

There paralegals in different fields, since lawyers have different specializations. You could work with a law firm that specializes in criminal cases, or one that handles civil cases. There are also divorce lawyers, family law practices, and others that specialize in disability claims.

The corporations often have a need for paralegals as well. Since many companies are engaged in highly regulated industries, they need to perpetually research regulations and changing laws. Even if you don’t have a specific legal background, your research skills gained from years of teaching, to make you a valuable asset in this capacity.

Becoming a paralegal usually requires obtaining a state-sponsored certificate. Since you’re a teacher, you almost certainly already have the education requirement covered, whatever it may be in your state of residence.

9. Sales

This is a career field that most teachers probably don’t think of. And in truth, people, in general, tend to shy away from sales. But if you’re people-oriented, sales can work well for you. And once again, if you have a pension and distributions coming out of your pension plan, you won’t have to deal with the income insecurity issue that plagues most commission-only salespeople.

While the idea of sales itself may not be terribly appealing, it may be a good fit if for you if it involves selling a product or service that you truly believe in.

One other major advantage of sales is that it is often the first step into a new career. After all, if you can be on the front lines selling a product, you could eventually move up the chain and into something totally unrelated within the field.

Once again, your ability to present before groups will be a definite advantage. But like tutoring, you’ll have to refine that down to a one-on-one presentation process. That’s because most of your sales presentations will be either to an individual, or to a very small number of people at the same time.

You may also find that your research skills will help you to gain product knowledge. Though we often think of sales as being the ability to out-talk customers, it’s really mostly about overcoming objections. If you have strong product knowledge, gained from research, you’ll be able to overcome those objections with little trouble.

Final Thoughts on Post-Retirement Careers for Teachers

If you decide that you want to retire, but only to retire from teaching, you have plenty of options. Your lifelong career as a teacher is giving you the kinds of skills that can easily move you into closely related- or even entirely different-career fields.

You could very well become a four-income person in retirement, benefiting from your pension, Canada Pension, Registered Retirement Income Fund (RRIF) income, and the income from a post-retirement career.

That’s more income potential than most people have going into retirement.

Firstly, this is a biased article for me to write as I am a financial advisor. However, when I talk to teachers at various points in their career about their financial concerns, the one response I seem to hear is “I wish I had one of you earlier”.

Why do teachers need a financial advisor?

1. Mistakes cost money

I recently came across a situation where a teacher needed money for an unexpected expense for her child. She didn’t have anyone to discuss the situation with, so she took money out of her RRSP to pay for the situation. She thought her situation made her eligible for “hardship withdrawal”.

It didn’t.

Not only did this withdrawal incur a penalty but the total amount was added to her annual income and subject to income tax.

If she had someone to discuss the situation with, and lay out all of her options, she would have realized that there were a number of other options available.

2. Uninformed choices cost money

I tell (almost) every new teacher to avoid RRSPs when saving for retirement. As a teacher, you will receive a pension in retirement. Income for your RRSP will increase the amount of money you will pay in taxes to Canada Revenue (CRA).

For most new teachers, RRSPs may appear appropriate because it’s likely what your parents or non-teacher friends are using. As your teachers’ income grows your pension adjustment will also reach its maximum. Your Pension adjustment limits the amount of contribution room available towards your RRSP.

When my wife and I bought our house, we pondered if we should buy a move-in ready townhome and move out when our family grew, or if we should buy a bigger house and do some work. We didn’t really ask people’s opinion who had been there before us and we bought the townhome.

After we bought, the housing market took a downturn and our sizable down payment (now in the form of equity) disappeared, meaning we were stuck for a while. Sometimes we look back and wish we had bought a different house. What if we had spoken to a young family or realtor to get their opinion before buying?

Before you make any initial moves, or changes, to your financial endeavors – have you asked anyone’s opinion? Have you asked a teacher who’s been in your situation recently, or a financial advisor (not sales-person)?

I would suggest you do, so you don’t look back in a couple of years, and think “What if?”

4. I could fix my toilet, but I don’t have a weekend available to do it

Some teachers I come across are knowledgeable about financial topics. They understand pension eligibility and what accounts work well with a pension in retirement. They understand insurance, and the basic estate planning documents they need in place, and the list of other financial things that occur in their lives.

But first and foremost, they’re teachers. They are experts at educating children, providing differentiation of content to various students, and explaining complex situations with ease. While they could manage their financial lives adequately, should they be?

How much time would it take, and how accurate would it be?

I think the same thing when any type of outlet or pipe breaks in my house. I can do some things in the house, but when it comes to anything plumbing or electrical, I know enough to hurt myself and spend hours getting to that point. It makes sense to pay a professional who can do it in 25% of the time, fix the problem completely, and keep me from harm. I’m happy to pay them for their expertise.

That’s what a good financial advisor does.

They know lots of options when it comes to products, approaches to investing, insurance and income tax management; study these topics to remain up-to-date, can design a comprehensive plan that can change your future, and know the danger areas to look out for.

As I said at the start, this is a biased article for me to write as I earn my living as a financial advisor. I work with teachers and help them maximize their lives; make things easy to understand and provide you the flexibility to enjoy your free time as you wish.

The Life Insurance Agent of Canada: There are various different types of life insurance available, but how do you know which one is right for you? Once you’ve found the right product, how much should you buy?

Do I need life insurance?

Are you married, have children, a mortgage, or other outstanding debts? Chances are you need some life insurance to assist your dependents should you pass away. (If you don’t have some of those things, don’t assume you don’t need life insurance.)

Take a typical family – husband, wife, and two kids. If the husband passes away, the wife is left with one income to provide for the three of them. One income to pay for everyday expenses, save for college, two growing children, and fund a future retirement. If there was a lump sum of money (Tax-Free) available to cover most (if not all) of these costs, that would be ideal.

Life insurance was designed for this primary need. It’s about maintaining the quality of living for the surviving family members and it’s not just paying down debt or living expenses. Consider the impact on children if the home needs to be sold because it is unaffordable for the surviving spouse. Moving to a lower-income neighbourhood, and changing schools all cause anxiety and leave hidden scars. Adequate Life insurance provides cash and that cash provides better choices.

I have some life insurance coverage from the school board. Do I need more?

While it’s true life insurance is available through the school board, it’s not nearly enough to cover all your needs such as; debt retirement, funeral expenses, living expenses, housing expenses, daycare, future education costs even retirement needs.

With the high cost of housing prices in Canada, many people need at least $1,000,000 in coverage to cover their family’s future costs, lost income and lost retirement savings.

How much do I need?

This depends on who you are, what life stage you’re in, what debts you have, and what goals you’re working towards! It is a custom situation for everyone, and one size rarely fits all. Most financial professionals use calculators to determine how much insurance their clients require.

For many people who are trying to use a rule of thumb, you should aim for between 10x-20x of your annual salary in coverage. But of course, this can be a wide range, so some custom analysis is always the best way to go.

Once you have an idea of how much you need, the cost of getting this insurance can vary widely depending on the type of insurance you buy.

What kind of insurance to buy?

There’s two kinds of life insurance: Term and Permanent

Term – this is purchasing pure insurance for a period of time. If you are 30 years old and want to insure yourself until you are 60, then you’ll purchase a 30-year term policy.

A level-term policy will keep the premiums the same throughout the 30-years (recommended), but once you reach 60, that insurance will go away (or get a lot more expensive). Term insurance is the lowest cost method of covering a large goal over a relatively short period. Term insurance is the highest cost of insurance to use at older ages say above 50 to cover final needs such as funeral and estate taxes. Permanent insurance is more cost-effective for those goals especially as final needs expenses rise over time.

Permanent – Permanent insurance comes in various forms – Whole Life & Universal Life. These are variations of a life insurance policy with a savings account (“cash value”) attached to it. Whole Life policies have a fixed amount of growth to the cash value (i.e. 5%).

Universal Life can assign these savings to segregated funds so it has the potential to grow faster or do a fixed rate of return. It also provides a lower premium than whole life.

These policies can get confusing very quickly, and there seems to be a limitless amount of riders (additional benefits) that can be added to these policies. They play a vital role in your financial plan during estate planning or as an alternative investment.

Who do I buy it from?

If you have an insurance agent that you work with, many of them are qualified to sell life insurance. If they only present insurance from one company ask why? Some companies pay more to advisors to sell their products. It’s ok to ask the advisor to disclose their compensation to you. In fact, it may reveal the motivation for recommending that particular insurance solution.

What do you recommend?

Insurance should always be considered by completing a comprehensive insurance needs analysis. Situations are different for everyone and implementing the wrong insurance solution can have devastating consequences. I do believe everyone should have insurance, rich & poor alike all have a need.

In 20 years of providing insurance solutions, I’ve been in many homes where the family never increased their insurance coverage since the first time they bought it. Think of your grandparents buying $10 thousand of coverage when homes were only $20,000. Many of them never bought insurance as their family expanded and their needs grew. Sadly, some of those families desperately needed more money at their passing.

There’s a saying our business; “I’ve never met a widow who complained the death claim was too much.”

Situations when contributing to an RRSP isn’t worth it

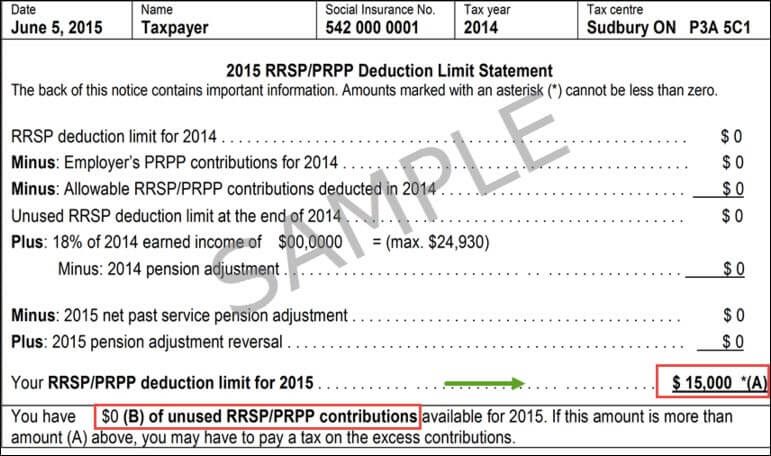

Your Ontario Teachers’ pension benefit is linked to your RRSP contribution room.

The greater the value of your pension benefit, the less room you will have available to contribute to an RRSP.

Every member of a registered pension plan receives an annual pension adjustment (PA). Your PA, which appears on your T4, reflects the value of the pension benefits you earned in a year. This is the Canada Revenue Agency’s (CRA) way of leveling the playing field between those who are members of a defined benefit pension plan and those who must rely solely on RRSPs for retirement income.

You can find your RRSP contribution room on the Notice of Assessment provided by the CRA each year.

Payout

Teachers receive a pension based on their years of service and their best five years’ average salary. A teacher who retires with a full pension worked for 32 years and earned a best-five-years average salary of $60,000 would have a basic pension of $38,400. A teacher earning $90,000 a year with 32 years of service would have an annual pension of $57,600. The pension amounts are reduced once teachers are old enough to begin collecting CPP payments because the teachers’ pension plan is designed to be integrated with CPP.

When does an RRSP not make sense?

When you expect to be in a higher tax bracket when you withdraw the funds.

If you have higher taxable income when you withdraw the funds, then you could be paying a higher rate of tax.

Start by getting a Second Opinion Portfolio Review to map out your retirement plans, you might not realize how the various income sources integrate. Focus on these particular areas; what, where, when & how much are the income streams at retirement? When will you start to use your retirement assets? Where will this income stream come from – Pension, RRSP, TFSA, savings, investment properties, private mortgages? What type of income is it – pension income, dividend income, interest income.

The average age of retirement for teachers is 57 although in recent years its been 61. Many teachers find that age too early to stop working and decide to open a business or become a consultant. This while being a great idea to keep busy, will also compound your tax issues at retirement.

When you have a sizeable employer plan or other taxable income sources.

If your employer has a pension plan available, then your already going to build a taxable income stream in retirement. Adding an additional taxable income steam such as an RRSP will only contribute to paying more income tax. As a teacher, your pension adjustment will limit the amount you can contribute to an RRSP anyway.

Many people weigh their RRSP contribution by how much they’re getting back from CRA. Retirement planning is a long-term approach. Utilizing a Goal-Based Planning approach shows you how much you should contribute to achieving your income needs at retirement. It’s a completely different way of thinking. ~ David Aaron

As mentioned previously, having additional income streams at retirement is ideal however, you want to plan ahead as to how to mitigate the tax treatment of those income streams.

What teachers are saying about David

I’ve been a teacher for 12 years and I’ve just always put my allowable limit into my RRSP. After meeting with David, he showed me how to continue funding my retirement using the same amount of money, while not increasing the amount I’ll have to pay to Revenue Canada. Honestly, when David showed me this, I was shocked no one had told me about this before!

Randy

Teacher PDSB

Everyone knows being a teacher your going to have a good pension when you retire but I wasn’t sure where to put the extra money I had for savings. An RRSP seemed to be the only option. I had no idea there was an alternative until I met with David. He took his time to explain how it worked and showed me the difference of using this strategy against the RRSP. Can I say my mind was blown! Thanks David.