COVID-19 Cash flow management strategies

Financial survival has been top of mind for many business owners since the first lockdowns were declared in March of 2020. Almost 40% of Canadian entrepreneurs are now trying to balance rebuilding their financial health against business needs

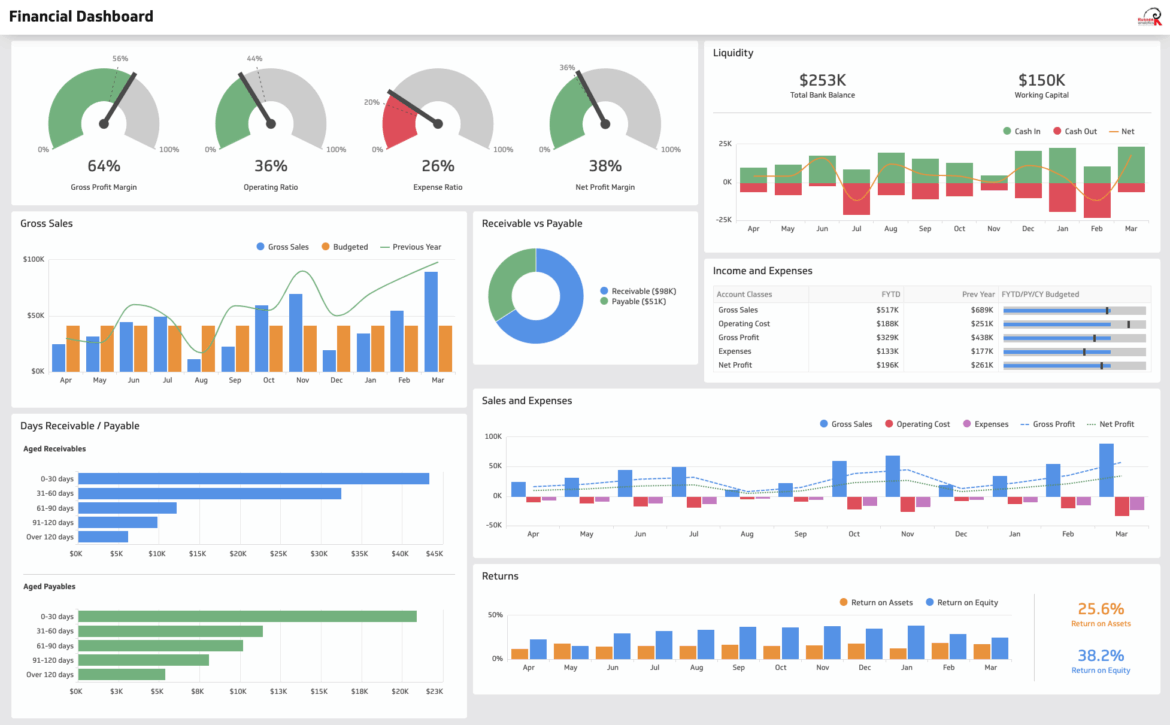

How to manage your finances to ensure the continuity of your business?

Here are few cashflow strategies that will help your business survive during time of economic downturn or catastrophic events such as COVID-19.

1. Agility is key

Business owners who are agile can pivot their operations and optimize their sales reducing the impact of the economic slowdown.

2. Lower expenses

Lowering expenditures to reflect reduced revenue can help businesses break even and keep their doors open.

3. Operate safely

Your customers need to be protected and feel safe to do business with you. Your employees must have a safe work environment. Ensure your communications are clearly marked for customers and your employees are well trained.

4. Curtail unnecessary spending

Watching your margins during any reduced revenue period is critical. COVID-19 in a way, has been a live exercise in business survival. Stay on top of accounts receivables and manage your payables to the latest date possible. Negotiate longer payable terms where possible e.g. ask to move from 30 days to 60 days.

5. Plan ahead

OK, this one seems common sense although, when your busy fighting fires it’s easy to get caught up in the “right now.” Some of those fires are showing up because you didn’t plan far enough ahead. Get in front of your problems and forecast further out.

What’s Your Business Interruption Strategy?

Many years ago, we had a 120 seat cafe/restaurant with a liquor license that was extremely successful. Literally a line at the door. So busy in fact, I slept on a cot in the back (closed at 2 am and opened at 8 am) during our 1st year.

When the sun is shinning you’re not thinking about umbrellas!

~ David Aaron

It was August, our busiest month of the year and construction had began in the parking lot to remove an old building to make way for additional parking. The construction company accidentally cut the water main flooding the parking lot. The entire parking lot was closed off and torn up. They piled mounds of pavement, stone and dirt right in front of our business. You actually couldn’t see our business. Sales revenue in August was normally $80-90,000…we did $6,000!

The landlord provided a $1,700 credit towards our lease and do you think that made any difference? We never considered planning for such an event. We had 16 employees, perishable food inventories and just like that disaster!

Planning for the worst case scenario

1. Break-Even Analysis

Add up all your fixed expenses such are lease, salaries, communications, interest and principal payments on loans. Then, divide this by the margin you earn on each sale (usually a percentage).

If you think your business might not earn break-even levels, you may have to consider cutting your expenses to the strict bare minimum. Consider temporarily removing products/services which are unlikely to break-even during this period.

2. Do some “Spring Cleaning”

Time to sell anything you haven’t used a long time and will unlikely ever use it. Such things as, equipment & vehicles. Cash is king here! Examine where you can get short-term financing.

3. Renegotiate fixed costs

For our restaurant, we negotiated with the landlord to reduce the lease over a several months and increase the lease payment during our higher business volume. Examine if this is possible with your business. Heating & Air conditioning is one are to consider. Adjusting the temperature by 1-2 degrees over time reduce your energy bill. While it may be a little uncomfortable, the alternative is far worse.

4. Change Your Pricing

Modify your pricing on items with the highest margin to increase the margin. One example in our restaurant was, in the winter strawberries are very expensive comparative to the summer. We increased our price for a top selling menu item by a nominal amount and removed strawberries from the menu. Instant boom to our bottom line.

5. Flexible Working Arrangements

Can you work from home or move to a co-working space to transform fixed rental costs into variable costs. Can any employees work from home?

6. Pay attention to giving out credit

Scrutinize new clients on their credit worthiness. When sales volume is low you don’t want to take on a delinquent new client. Also keep a closer eye on customers who are falling behind with their bills. Ask for a partial payment to mitigate a larger delinquency – receiving some cash during these times is better than none at all.

7. Establish and maintain strong credit

“But I don’t need credit right now.” Establishing lines of credit is essential in business. Even General Electric ran out of credit during the 2008 financial crisis. Using credit during normal business cycles is good financial management. Having access to credit during economic contraction is critical to business sustainability.

8. Death by a thousand cuts

Pay attention to the small almost invisible expenses. They can add up to quite a bit:

- Subscription services for social media platforms. LinkedI n is $100 per month for Sales Navigator. Perhaps a pause on this and similar accounts is necessary

- Paid advertising – if you have modified your product/services discontinue ads which are promoting those items

- Data charges – If business volume is low do you need to have the highest data package?

- Infrastructure costs – During COVID-19 you’ve been paying for infrastructure to support a business at 80-110% volume when in fact you may have been at 20%. You need pivot quickly to reduce these costs.