Divorce and Money – Our Guest speaker Maureen Catherine Tabuchi, LL.B., MTax discusses the impact of divorce on Business owners and individuals. Divorce can often have devastating financial consequences for one or both parties.

The majority of marriage breakdown occurs between September and New Year’s Day. In fact, the first Monday after Christmas or New Year’s Day is when married couples would settle on a split, and when September ends is when separations are most commonly agreed upon.

Divorce and separation can be a difficult time for everyone. It is important to know your rights, obligations, and options before making any decisions that will have an impact on you or your family’s future.

If you are going through a divorce or separation from your spouse it’s important to work with a law firm that understands what your going through. Maureen’s team of experienced lawyers provide legal services including negotiating and drafting Separation Agreements; Representation in Mediation or Arbitration; Legal advice about spousal support (alimony), child custody & access (Visitation), child support, property division, possession of the matrimonial home, equalization of assets; Family Law litigation including Parenting Plans (Parenting Arrangements) & Child Protection Orders (Child Custody); Enforcement proceedings under The Family Maintenance Act; Advice regarding related issues such as Matrimonial Property Division Tax Planning, etc.; Preparation for Court Hearings if required by attending court with our clients.

The majority of marriage breakdown occurs between September and New Year’s Day. In fact, the first Monday after Christmas or New Year’s Day is when married couples would settle on a split, and when September ends is when separations are most commonly agreed upon.

Divorce can often have devastating financial consequences for one or both parties. If you’re required to pay as part of your separation agreement or divorce, consider carefully which accounts to use.

Do Not Do Make a Withdrawal from Your Tax Free Savings Account to Pay for a Marriage Breakdown

When there is a breakdown in a marriage or common-law partnership, an amount can be transferred directly from one individual’s TFSA to the other’s TFSA without affecting either individual’s contribution room.

The transfer must be completed directly between the TFSAs by the issuer. If you are in this situation, you must meet both of the following conditions:

you and your current or former spouse or common-law partner were living separate and apart at the time of the transfer

you are entitled to receive, or required to pay, the amount under a decree, order, or judgment of a court, or under a written separation agreement to settle rights arising out of your relationship on or after the breakdown of your relationship

When these conditions are met, the transfer is a qualifying transfer and will not reduce the recipient’s eligible TFSA contribution room. Since this transfer is not considered a withdrawal, the transferred amount will not be added back to the transferor’s contribution room at the beginning of the following year.

Also, the transfer will not eliminate any excess TFSA amount, if applicable, in the payer’s TFSA.

Take a moment to think of every account you need a password to access. You’d have to add up all the apps on your phone, think of every online profile you’ve created, remember pins and bank account passwords. Today, passwords have become so commonplace that it’s easy to take their purpose for granted. However, keeping passwords secure prevents hacking and is essential to digital and financial security.

Passwords and password hacking

Most online and digital profiles these days rely on a username and password combination to verify user identity. To ensure these profiles remain safe and confidential, well-crafted passwords are essential.

The rising prevalence of password hacking to enter confidential or financial online accounts, in particular, has made password security extremely important. Weak or common passwords make access to digital profiles easy for hackers, who use sophisticated programs to uncover passwords and hack accounts.

Creating a strong password

In order to create a password that lessens the likelihood of being guessed or hacked, consider the following:

Common words make poor password choices on their own. Try using special characters (@, #, $, &, etc.) in place of letters or numbers.

Use a minimum of eight characters in your password with a combination of lowercase letters, capital letters, numbers and special characters.

Unusual combinations work best. One option is to make an acronym using the first letter of each word in your favorite song lyric.

For maximum protection, you can simply type random letters on a keyboard. Because this will be very difficult to remember, see below for some ideas on how you can store your password securely.

Have different passwords for different devices, applications, online accounts and systems.

Don’t use personal information in your password that can be easily accessed or guessed (such as birthdays or pets’ names).

Change your password regularly. When you do change the password, try not to repeat the same set of words, such as password1, password2.

Replace the weak or duplicate passwords with stronger, unique passwords.

It can take some time to collect all of the necessary income information, so be sure to give yourself plenty of time.

Secure password storage

With so many passwords and login combinations, many users have difficulty remembering their passwords. We recommend the following to help you keep track:

Do not write passwords down on slips of paper or in a notebook. These items are easily lost or stolen. If you do need to write down your passwords, don’t include the account user name with them.

Save your password in a text file, then save the file on a password-protected, encrypted USB drive.

Consider a password management program. Many offer high-quality password management features. For instance, you can use the software to generate and store secure passwords on your behalf.

Learn about cookies. A cookie is a personalized bit of data that internet browsers use to identify returning users to a site. If your browser remembers you, you can more easily gain access to your digital profiles each time you go to a frequently visited site. That way, you don’t have to re-enter your info every time.

Likewise, most browsers allow users to save your login information within the browser. This saves you from needing to frequently re-enter your password. Be aware, this information can be lost if you delete your cookies. As a result, you should not rely solely on internet browsers for password tracking.

Passwords can never be completely safe from discovery. However, by following the steps listed above, you can drastically reduce the likelihood of having your password uncovered.

Moving the needle forward on becoming financially independent doesn’t mean doing all of these tips, although why not try adopting 1 or 2 each month. From the best ways to budget to how to boost your earning potential like a pro, these tips of financial wisdom are sure to get you headed in the right direction.

First Things First: A Few Financial Basics

1. Create a Financial Calendar

If you don’t trust yourself to remember to pay your quarterly taxes or periodically pull a credit report, think about setting appointment reminders for these important money to-dos in the same way that you would an annual doctor’s visit or car tune-up.

✅ TIP: Consider making a list of your bills and due dates. Leave it out where you see it every day and make a note of when and how much you paid towards the bill. Visually you will see which bills you forgot to pay this month. To keep a good credit score, don’t miss paying at least the minimum due each month.

~ David Aaron, Aaron Wealth Management

2. Check Your Interest Rate

Q: Which loan should you pay off first? A: The one with the highest interest rate. Q: Which savings account should you open? A: The one with the best interest rate. Q: Why does credit card debt give us such a headache? A: Blame it on the compound interest rate. The bottom line here: Paying attention to interest rates will help inform which debt or savings commitments you should focus on.

3. Track Your Net Worth

Your net worth—the difference between your assets and debt—is the big-picture number that can tell you where you stand financially. Keep an eye on it, and it can help keep you apprised of the progress you’re making toward your financial goals—or warn you if you’re backsliding.

How to Budget Like a Pro

4. Set a Budget, Period

This is the starting point for every other goal in your life. Debt can creep up on you. It’s so easy to accept small financial obligations in today’s society with smartphones. Some of those apps on your phone are free while others have a small monthly fee. Netflix’s basic plan is only $10 per month, so are many other fun and useful apps. Next thing you know you’re into hundreds of dollars in monthly obligations.

✅ TIP: Consider looking at your life as a business or corporation. You can only spend what you earn and you also need to conserve cash for future growth and for rainy days.

~ David Aaron, Aaron Wealth Management

5. Consider an All-Cash Diet

If you’re consistently overspending, this will break you out of that rut. Now, this is a little harder to do given many companies want a credit card just to open an account. Try renting a car without a credit card for example. The benefit of paying cash for as many things as possible is being hyper-aware of what you’re spending your money on.

6. End of day money review

At the end of your day take a couple of minutes to review what you spent money on (Hopefully one bill was a deposit to your savings). This reflection helps to identify problems or negative patterns immediately and keeps track of goal progress.

✅ TIP: You make XX amount of money each year. The moment you buy something you’ve given up that money. It’s gone forever. Ask yourself this question: How does this purchase add value to my life?

~ David Aaron, Aaron Wealth Management

How to Get Money Motivated

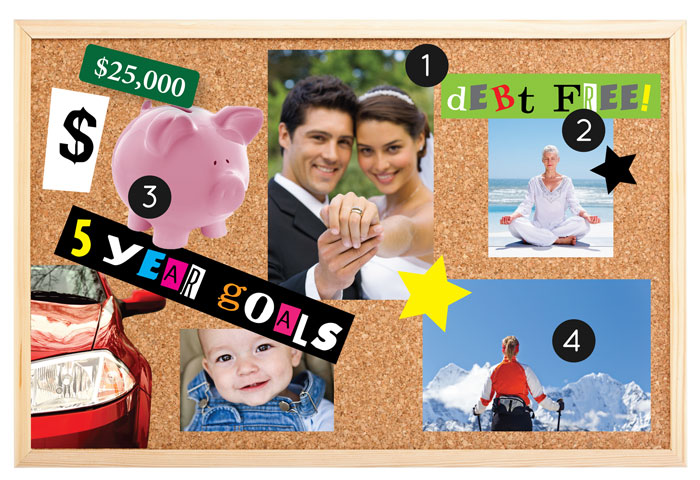

7. Create a Financial Vision Board

You need the motivation to start adopting better money habits, and if you craft a vision board, it can help remind you to stay on track with your financial goals. More than that it’s a psychological trick ( a healthy one). Your subconscious mind will work day and night (that’s right, even when your sleeping) to bring these images into reality.

8. Set Specific Financial Goals

Use numbers and dates, not just words, to describe what you want to accomplish with your money. How much debt do you want to pay off—and when? How much do you want saved, and by what date? Napoleon Hill’s book “Think & Grow Rich” has a chapter which in my opinion is one of the best step-by-step processes to helping you achieve any goal, especially financial goals.

9. Make Bite-Size Money Goals

One study showed that the farther away a goal seems, and the less sure we are about when it will happen, the more likely we are to give up. So in addition to focusing on big goals (such as, buying a home), aim to also set smaller, short-term goals along the way that will reap quicker results—like saving some money each week in order to take a trip in six months.

1o. Banish Toxic Money Thoughts

This has everything to do with your internal dialog and how you view money. Negative thoughts and spoken words have power. Cut them off right in there tracks.

✅ TIP: Be mindful of your thoughts and choose your words carefully. Karma is the energy created by thoughts and words. Careless thoughts & words will produce negative energy. Good thoughts & words produce good energy. If you want good things to show up in your life, cut out your negative thoughts & words.

~ David Aaron, Aaron Wealth Management

11. Get Your Finances–and Body—in Shape

One study showed that more exercise leads to higher pay because you tend to be more productive after you’ve worked up a sweat. So taking up running may help amp up your financial game. Plus, all the habits and discipline associated with exercising are also associated with managing your money well.

12. Appreciate what you have

Do you have clothes hanging in your closet with tags still on them? Maybe it was an impulsive purchase or you couldn’t pass up a sale. Being content with what you already have is not only a healthy state of mind, it will also slow your impulsive spending.

How to Amp Up Your Earning Potential

13. When Negotiating a Salary, Get the Company to Name Figures First

If you give away your current pay from the get-go, you have no way to know if you’re lowballing or highballing. Getting a potential employer to name the figure first means you can then push them higher.

14. You Can Negotiate More Than Just Your Salary

Your work hours, official title, maternity and paternity leave, vacation time, and which projects you’ll work on could all be things that a future employer may be willing to negotiate. Employers have learned lessons from COVID-19 and are more inclined to have employees work from home. This is a huge saving for employees in areas such as; transportation, dining out, work clothes, and even time. Yes, time is money.

15. Make Salary Discussions at Your Current Job About Your Company’s Needs

Your employer doesn’t care whether you want more money for a bigger house—it cares about keeping a good employee. So when negotiating pay or asking for a raise, emphasize the incredible value you bring to the company.

How to Keep Debt at Bay

16. Start With Small Debts to Help You Conquer the Big Ones

If you have a mountain of debt, studies show paying off the little debts can give you the confidence to tackle the larger ones. You know, like paying off a modest balance on a department store card before getting to the card with the bigger balance. Of course, we generally recommend chipping away at the card with the highest interest rate, but sometimes psyching yourself up is worth it.

17. Don’t buy too much house

This happens when you fall in love with a house where your mortgage is near 30% of your take-home pay. You’re going to curse that house you fell in love with when your not able to enjoy living because you have no money left.

How to Shop Smart

18. Evaluate Purchases by Cost Per Use

It may seem more financially responsible to buy a trendy $5 shirt than a basic $30 shirt—but only if you ignore the quality factor! When deciding if the latest tech toy, kitchen gadget, or apparel item is worth it, factor in how many times you’ll use it or wear it. For that matter, you can even consider cost per hour for experiences!

A good example of this is your bedroom. You’re going to spend about a third of your life in bed and getting a great sleep is immeasurable. We waited for the bedroom set we loved to go 50% off. It cost us $13,000 and we kept it for 14 years. Sounds crazy to calculate this but…it cost us $2.55 to sleep each night over those 14 years!

19. Spend on Experiences, Not Things

Putting your money toward purchases like a concert or a picnic in the park—instead of spending it on pricey material objects—gives you more happiness for your buck.

20. Go shopping by yourself

Ever have a friend declare, “That’s so cute on you! You have to get it!” for everything you try on? Save your socializing for a walk in the park, instead of a stroll through the mall, and treat shopping with serious attention.

How to Save Right for Retirement

21. Start Saving NOW!

Not next week. Not when you get a raise. Not next year. Today. Because the money you put in your retirement fund now will have more time to grow through the power of compound growth. Albert Einstein said, “Compound Interest is man’s greatest invention.”

22. Do Everything Possible Not to Cash Out Your Retirement Account Early

Dipping into your retirement funds early will hurt you many times over. For starters, you’re negating all the hard work you’ve done so far saving—and you’re preventing that money from being invested. Second, you’ll be penalized for an early withdrawal, and those penalties are usually pretty hefty. Finally, you’ll get hit with a tax bill for the money you withdraw. All these factors make cashing out early a very last resort.

22. Get that free cash

Take advantage of your employer’s group retirement plan as many plans match your contribution (to a maxed percentage). But you’ll only get that contribution if you contribute first. Another hidden advantage is the fee for investing. Group plans tend to have very low investment fund fees (under 1%). To get these low fees outside your group plan you would either need a lot of money to qualify for a lower fund fee or invest in index funds & Exchange Traded Funds (ETF). A group plan solves that issue for you.

23. When You Get a Raise, Raise Your Retirement Savings, Too

You know how you’ve always told yourself you would save more when you have more? We’re calling you out on that. Every time you get a bump in pay, the first thing you should do is up your automatic transfer to savings, and increase your retirement contributions. It’s just one step in our checklist for starting to save for retirement.

Building credit

24. Review Your Credit Report Regularly—and Keep an Eye on Your Credit Score

This woman learned the hard way that a less-than-stellar credit score has the potential to cost you thousands. She only checked her credit report, which seemed fine—but didn’t get her actual credit score, which told a different story.

25. Keep Your Credit Use Below 30% of Your Total Available Credit

Otherwise known as your credit utilization rate, you calculate it by dividing the total amount on all of your credit cards by your total available credit. And if you’re using more than 30% of your available credit, it can ding your credit score. If your interested in having the best score keep your utilization rate below 10%.

26. If You Have Bad Credit, Get a Secured Credit Card

A secured card helps build credit like a regular card—but it won’t let you overspend. And you don’t need good credit to get one!

How to Get Properly Insured

27. Get More Life Insurance on Top of Your Company’s Policy

That’s because the basic policy from your employer is often far too little and if you get fired so too is your life insurance. There are usually provisions to continue your insurance although the price is not as competitive as getting your own. Life insurance will never be cheaper than it is today. Sounds like a sales phrase but seriously, it’s based on your age & health. It gets more expensive for you to buy as you age so lock in those premiums now.

28. Get Renters Insurance

It, of course, covers robberies, vandalism, and natural disasters, but it could also cover things like the medical bills of people who get hurt at your place, damages you cause at someone else’s home, rent if you have to stay somewhere else because of damage done to your apartment—and even stuff stolen from a storage unit. Not bad for about $30 a month!

Be Prepared for Rainy (Financial) Days

29. Make Savings Part of Your Monthly Budget

If you wait to put money aside for when you consistently have enough of a cash cushion available at the end of the month, you’ll never have money to put aside! Instead, bake monthly savings into your budget now.

30. Keep Your Savings Out of Your Checking Account

Here’s a universal truth: If you see you have money in your checking account, you will spend it. Period. The fast track to building up savings starts with opening a separate savings account, so it’s less possible to accidentally spend your vacation money on another late-night online shopping spree.

✅ TIP: Grant Cardone says, “Get Broke each month. Get rid of your savings. You can’t save your way to being wealthy. You need to get it invested as quickly as possible.”

Why, you ask? Because it makes you feel like the money you shuttle to your savings every month appears out of thin air—even though you know full well it comes from your paycheck. If the money you allot toward savings never lands in your checking account, you probably won’t miss it—and may even be pleasantly surprised by how much your account grows over time.

32. Consider Switching to a Credit Union

Credit unions aren’t right for everyone, but they could be the place to go for better customer service, kinder loans, and better interest rates on your savings accounts.

33. There Are 5 Types of Financial Emergencies

Hint: A wedding isn’t one of them. Only dip into your emergency savings account if you’ve lost your job, you have a medical emergency, your car breaks down, you have emergency home expenses (like a leaky roof), or you need to travel to a funeral. Otherwise, if you can’t afford it, just say no.

34. Have 6 months of emergency cash

Rule #1. Pay Yourself First! Start saving right away into an account where this money will only be used in the case of an emergency as mentioned above. There are many opinions on the amount, although 6 months of expenses is appropriate.

How to Approach Investing

35. Pay Attention to Fees

The fees you pay in your funds, also called Management Expense Ratios (MER), can eat into your returns. Even something as seemingly low as a 1% fee will cost you in the long run. Index funds & Exchange Traded Funds (ETF) are the lowest fees on the market although bear in mind getting advice may be challenging as fees are used to pay for the advice. A low fee may mean no advice.

36. Rebalance Your Portfolio Once a Year

If you’re not getting advice from an advisor then you will need to do this yourself. I strongly recommend you use an advisor, studies show investment accounts with an advisor are higher as compared to no advice. What does Rebalancing mean? Let’s say you had allocated your portfolio to have 60% equities & 40% bonds. Throughout the year these values change because of gains or losses in your investments. At the start of the year, rebalance your portfolio to ensure you still have a 60/40 split.

Get the benefit of experience and knowledge from a team of seasoned professionals who can assess your needs and suggest appropriate strategies. Simply saving money isn’t enough – creating a financial plan with the help of professionals will help you achieve your goals much faster.

Borrowing too little or too late can jeopardize your business

Getting a business loan can be the fuel your company needs to reach the next level of success.

But you have to prepare yourself and your company to get the money and make sure the loan is right for you.

1. Borrowing too late

You may be tempted to finance your expansion projects from your cash flow. But paying for investments with your own money can put undue financial pressure on your growing business. You may find yourself needing to borrow money quickly and doing it from a position of weakness.

When there’s a sense of urgency, it usually indicates to a banker there was poor planning. It’s often harder to access financing when you’re in that position.

Solution—Prepare cash flow projections for the coming year that take into account month-to-month inflows and outflows, plus extraordinary items such as planned investments. Then, visit your banker and discuss your plans and financing needs so you can line up the funding before you need it.

2. Borrowing too little

You’re right to be careful about how much debt you take on. However, low-balling how much a project will cost you can leave your business facing a serious cash crunch when unexpected expenses crop up.

Solution—Develop a cash flow forecast for each individual project including optimistic and pessimistic scenarios. And then borrow enough money to ensure you can cover your project, unforeseen contingencies and the working capital required to bring your project to completion.

3. Focusing too much on the interest rate

The interest rate on your business loan is important, but it’s far from the whole story. Other factors can be just as important, or even more so.

What loan term is the lender willing to offer?

What percentage of the cost of your asset is your lender willing to finance?

What is the lender’s flexibility on repayments? For example, can you pay on a seasonal basis or pay only interest for certain periods?

What guarantees are being asked from you in the case of default? Do you have to pledge personal assets?

There are qualitative items in a loan agreement you have to think through very carefully. Some entrepreneurs will skim over the loan terms and conditions because they think they’re just legal jargon or standard terms requested by all lenders. But the truth is that terms and conditions can differ greatly between lenders.

Solution—Shop around among financial institutions for the most attractive package, keeping in mind the importance of the terms other than the interest rate.

4. Paying your loan back too fast

Many business owners want to pay back their loans as quickly as possible in an effort to become debt-free. Again, it’s important to reduce debt, but doing so too quickly can cost your business. That’s because you may leave yourself short of cash. Or the extra money you’re devoting to debt reduction might be better spent on profitable growth projects.

Solution—Compare your projected return on investment to how much interest you’re saving by paying down your loan faster than required. If you expect to earn more investing the money in your business, consider slowing down your repayment pace.

5. Failing to keep your financial house in order

It’s all too common for busy entrepreneurs to let record-keeping and other financial chores slide—with potentially disastrous consequences. It’s essential to keep good financial records, including year-end financial statements. Messy financial records can leave you in the dark about how your business is performing until it’s too late to take corrective action. It can also make it difficult to approach a banker for a business loan because not only do you lack documentation, but you’ve also shown a lack of managerial acumen.

Solution—Be diligent about keeping financial records and spend the money to hire an accountant. Also, consider getting help from a consultant who specializes in financial management to get your business on the right track.

6. Making a weak pitch to your banker

You can see how much sense your project makes, but you won’t get far if you can’t persuade your banker to get on board. MacKean says too many entrepreneurs are unable to clearly explain their company’s business plan, past performance, competitive advantages, and proposed project. The result is a polite “no, thanks.”

Solution—Prepare your pitch and practice it repeatedly. Focus on explaining your business and how you’re going to use the money you want to borrow in clear and compelling terms. Remember a big part of your sales job is persuading your banker to have confidence in your management smarts and ability to build a strong business (and pay back the loan).

7. Depending on just one lender

Having a relationship with just one financial institution can limit your options, especially if your business hits a bump in the road. You don’t want one lender holding all the cards should something go wrong. So, just as you would diversify your suppliers or customer base, or your own personal investments, you want to diversify your lending relationships.

Solution—Meet with other lenders and consider using different institutions for different types of financing products.

Preparing an effective, well-documented commercial loan proposal is the first step toward getting the money your business needs from a bank.

Your small business loan proposal will often be the first contact a banker has with your company. So you need to craft a document that presents your business in the best possible light.

The goal is to persuade the banker that you’re ready and able to make a success of your business and repay the loan.

Your business plan is key

The key part of proposals for small business loans is the business plan. Take the necessary time to do a thorough job of preparing it, ensuring it covers the following sections.

Executive summary—This section provides a concise overview of your business. It briefly describes your company, its industry, and its competitive advantage. It should also describe the business need or project that requires financing, as well as the amount of money needed.

Description of the company—In the main part of your business plan, you should more fully describe the history, current operations and strategy of your business.

Management team experience—Show the skills, experience, and qualifications of each member of the management team. Your banker needs to know they have what it takes to make your project work.

Key financial data—This section shows the financial strength of your business. Provide financial statements as well as forecasts for the next 2 to 3 years. Your banker will examine this information closely in an effort to understand your track record and capacity to repay the loan. As in every part of your small business loan proposal, make sure you are completely honest and transparent.

Marketing plan—Provide a marketing plan to answer these key questions: Is there a proven market for your product or service? Who are your competitors and what are their strengths and weaknesses? What is your client profile? What is your key competitive advantage?

Production plan—Your banker will want to know if you have the operational capacity to handle your projected sales.

Human resources management—Demonstrate that your business has the ability to recruit, develop and retain the right people to move your business project further.

Include supporting documents

You should bolster your commercial loan proposal by including documents that support, explain and boost the credibility of your plan, including:

market studies or other research supporting your conclusions and forecasts;

documents to support financial data (e.g. copies of leases, subcontractor estimates, letters of credit);

client testimonials; and

media reports about your company.

The purpose of the supporting documents is to show your proposal is based on facts.

Tips to write an effective commercial loan proposal

Use simple, plain language. Avoid technical terms and acronyms. Your proposal should be clear, well-structured and easy to read.

Don’t forget that your proposal’s purpose is to show your company at its best. Sell yourself!

Throughout the proposal, focus on showing why your venture will succeed. Demonstrate that you’ve thought of multiple possible scenarios and that you have contingency plans.

Image counts. Consider working with a professional to help you to layout the document. If writing isn’t your strength, ask for the help of a professional copywriter or editor.