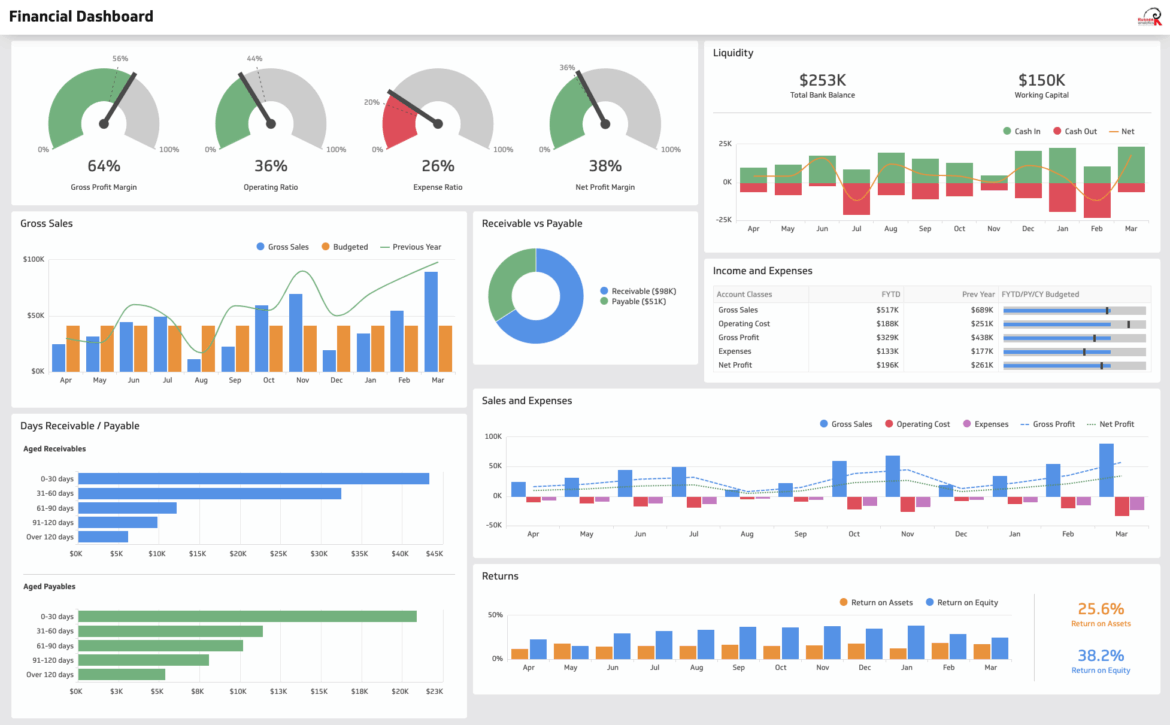

Financial dashboards

Find out how your business is doing and quickly reveal variations that might require corrective action with these important indicators.

Monitoring your cash flow is one of the best ways to improve the financial health of your business. It could mean the difference between going through some financial bumps and having to close your business.

Creating a spreadsheet and updating it regularly will provide you with the data you need to create your financial dashboard—a group of indicators used regularly to monitor your company over time that will tell you how you’re doing and quickly reveal variations that might require corrective action. (Accounting software often offers a dashboard as part of its cash flow management tools.)

For better overall cash flow analysis, always start by making financial projections that reflect expected monthly inflows and outflows, including major anticipated purchases and financing. Then, use your spreadsheet to compare your projections to actual results.

Cash flow indicators typically found on a dashboard include:

- Actual sales and sales in your pipeline

- Average days collection (for your accounts receivable) and average days payable outstanding (to your suppliers)

- Inventory outstanding

Other indicators will depend on what type of business you are running.

Here are three important metrics you might want to consider also including on your cash flow dashboard.

1. Cash on hand

Some businesses monitor this number on a daily basis. If cash on hand falls below your target, alarm bells should go off and contingency measures taken.

Continuously monitor how much cash you have on hand and check it against the target set when you did your financial projections. Your quick ratio and your working capital ratio will tell you if you have enough cash on hand to meet short term needs.

2. Cash conversion cycle

Tracking this metric over time will help you identify sources of cash flow problems and measure progress in tightening your cash flow management. The lower this number, the better—it means you have more cash on hand to generate additional returns and/or reduce your line of credit.

To determine your cash conversion cycle take the number of days of inventory outstanding (how long it takes on average to sell your inventory), then add to it the number of days receivable outstanding (how long it takes your customers to pay you), then subtract the number of days payable outstanding (how long it takes you to pay your bills).

Formula

Cash conversion cycle =

Days inventory outstanding + Days receivable outstanding –Days payable outstanding

3. Gross profit

Gross profit is a great starting point for determining the value of every sale and making pricing and promotion decisions.

It’s important to keep an eye on it since a gradual decline could mean future trouble for your business.

Your gross profit (or gross margin) is the money you make directly from selling products and services, minus the cost of sales. It doesn’t include indirect cost of sales such as rent and marketing.

You can calculate your gross profit as a percentage of revenues using the following formula:

Formula

Gross profit margin = Gross profit / Revenues X 100