As a result of the pandemic, many businesses have had to adjust their way of thinking when it comes to working remotely. Larger companies have the technology, flexibility and overall resources to have their employees transition quickly to a work-from-home, remote setup. For small businesses that don’t have a history of managers and employees working from home, the “new normal” may pose more of a challenge.

Working in the age of COVID-19

This new way of working presents many challenges, such as distractions from children at home, lack of cohesion with team members, and an increased chance of miscommunication. But there are things you can do as a small-business owner:

Equip teams with the right technology

Manage remote employees by communicating often and with transparency

Maintain engagement and help with productivity by creating opportunities for social interactions

Equip your team with the right tools

One of the most important ways to stay productive and connected while teams are working remotely is to have the right technology. This includes project management tracking, messaging apps and videoconferencing apps. These tools allow managers and employees to stay on the same page no matter where they are. Here are a few resources you can access:

Communication is especially important because interactions are happening virtually, leaving more room for miscommunications. Ensure that you’re consistently communicating with your teams while working from home and getting feedback from them about what is working well and what is not. Here are a few tips to help:

Sending out daily or weekly emails with updates or instant messages about projects can help employees to feel in the loop and know what is happening

Set expectations for how often you will check in, and let employees know how much they should update you as well

It’s important to communicate when you will be available and when you expect employees to be online

Use other forms of communication —such as phone calls or video calls — instead of defaulting to only text-based communications

If you would have talked to someone face-to-face about something while in the office, give them a call

Tips for managers to help maintain social interactions

Managers should provide more opportunities for spontaneous workplace conversations. Utilizing technology can help facilitate these conversations:

Make time to connect with teams or even schedule online social time to have conversations with no agenda

Encourage workers to connect virtually as they would in person

Try an icebreaker during a team chat, such as:

“What’s one good thing that someone ready today?”

“What’s one way everyone is de-stressing right now?”

Implement a weekly virtual happy hour or team-building exercise to keep people connected

Working remotely can work

Nothing takes the place of interacting face-to-face with a co-worker. Hopefully, these ideas will help small-business owners feel better informed and prepared about how to manage their teams remotely during the pandemic. Plus, if a small-business owner decides to focus more on this “working remotely model” after the pandemic subsides, they’ll be well prepared.

Protect yourself and your business during the pandemic

These are harrowing times, but keeping informed can be one of the best ways to feel empowered. We want to highlight what to look out for and what we can all do together to help protect you and your business from cyberattacks.

The scams are out there

It’s hard to believe that people will take advantage of our current situation with the outbreak of COVID-19, but it’s part of the narrative. According to the Cybersecurity and Infrastructure Security Agency (CISA), cyber criminals could take advantage of public concern surrounding COVID-19 by launching cyberattacks. Scams began surfacing back in January with coronavirus phishing schemes and are on the rise.

Phishing attacks

The CISA notes phishing attacks, or the use of email and bogus websites created to trick victims into revealing sensitive information, will be used by cybercriminals looking to take advantage of COVID-19. 29% of business owners have fallen prey to phishing attacks, according to its 2019 Small Business Owner survey5.

Disinformation campaigns

Disinformation campaigns will also be used by cybercriminals, as COVID-19 creates an opportunity to spread fear, manipulate public conversation, influence policy development or disrupt markets. A disinformation campaign is typically used by cybercriminals to spread false information online. For example, a cybercriminal could share content about a fake government relief package for small-business owners. If the content is clicked on or downloaded, malicious software is spread on the user’s device.

Vulnerability of alternate workplaces

As organizations explore alternative workplace options in response to COVID-19, such as working from home, the security of information technology systems may be used by criminals to create cyber threats. Coronavirus-themed ransomware is being used to encrypt a computer’s hard drive, enabling hackers to demand payment to unlock the information and files it contains.

We did our own research

A Small Business Owner Survey found that remote workers are a leading cyber blind spot for small-business owners. This same study found that only 4% of business owners have implemented all of the cybersecurity best practices and recommendations outlined by the government.

Follow these guidelines

We looked at the best ways for you to protect yourself and your business from cyberattacks and here are 5 things you can do.

Tip 1: Combat phishing attacks.

Do not click on links in unsolicited emails, and use caution when opening attachments

Never share personal or financial information in email

Tip 2: Guard against disinformation campaigns.

Use trusted resources, such as government websites, for up-to-date information on COVID-19. Here’s a link to Canada.gov.ca COVID-19 topics.

Tip 3: Use secure internet connections.

Make sure you and your employees work only from secure internet connections. When accessing any confidential or sensitive information, avoid using public Wi-Fi networks.

Tip 4: Secure your business’s information technology systems that enable remote access.

Ensure your virtual private network (VPN) and other remote access systems are fully patched

Enhance system monitoring to receive early detection and alerts on abnormal activity; implement multi-factor authentication

Tip 5: Back up your systems to combat ransomware attacks.

Ransomware attacks are a type of malware threat that locks valuable digital assets and files until a ransom is paid to release them. You should:

Make sure you can restore your files should a ransomware attack occur by storing files offline and if possible, off-site

Keep several days’ versions of backups, so you can restore your files using malware-free copies

Keep in mind, while real-time backup is convenient, it won’t be effective if your files are encrypted, because the ransomware will encrypt your files on the real-time backup.

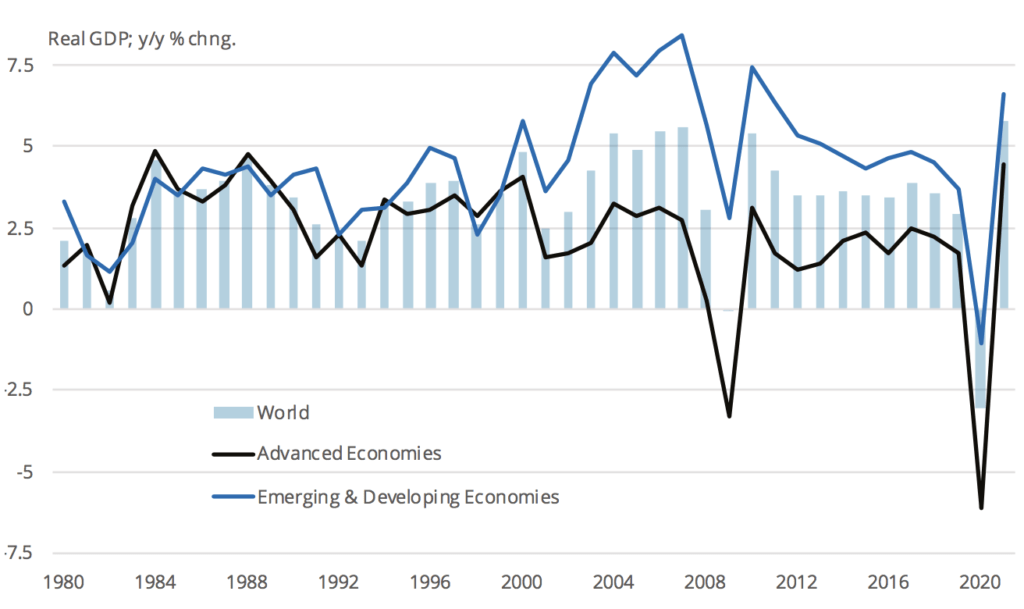

The global and Canadian economies are in the midst of the worst recession since the Great Depression.

The IMF is projecting the world economy will contract by at least 3 percent this year, a sharp reversal from growth of 3.3 percent anticipated in January 2020. To appreciate the severity of the current downturn, one need only consider that the global economy merely stalled (-0.1 percent) during the Great Recession of 2008/09 (see Figure 1). For advanced economies, like Canada, the downturn looks to be twice as deep as the 3.3 percent dip in 2009, while emerging economies in aggregate will experience the first decline in output on record. Fortunately, the tide appears to be turning, with growth expected to return in the second half of this year and through 2021.

The economic fallout has been dramatic to date. As the COVID-19 virus morphed from a local epidemic to a global pandemic, governments around the world implemented containment measures such as “stay-at-home” orders and shutdown non-essential businesses. Global trade stalled as economic shutdowns (existing or planned) severely disrupted supply chains and took a bite out of demand. The fall-off in demand exacerbated the imbalances in commodity markets and pummelled prices. Oil prices were particularly hard hit with supply initially relatively unaffected while demand plummeted as transportation ground to a halt.

One of the most unique and defining characteristics of this downturn is that, while both contracted greatly, service-producing industries have been more severely impacted than the goods-producing sector. The service sector’s high labour intensity and close human contact has only intensified the surge in the unemployment rate. The toll was particularly hard on lower paid service workers because of their high concentration in tourism, retail, hospitality, and food services industries. This downturn has also been harder on women, who make up a higher share of the workers in the most affected sectors.

The collapse in economic output and spike in unemployment have been swifter than ever before. Fortunately, so has the rapidity of the policy response. Around the globe, central banks have deployed significant monetary stimulus through lower interest rates and/or asset purchase programs. Monetary authorities have also injected liquidity in money markets to ensure the flow of credit. On the fiscal side, governments deployed income support programs for workers and financial aid to businesses. These actions helped lower the economic downside risks, including the risk of a protracted downturn (depression) and/or deflation.

Figure 1: Global economic growth over four decades

Don’t judge a recovery by its headlines

Due to publishing lags, often one to two months long, official economic statistics have only recently began to reveal the magnitude of the downturn. But, much of the world economy is in the process of reopening. There is now some evidence that the trough in economic activity (due to COVID-19) may have taken place in April. As such, the focus of policymakers has shifted from ‘responding’ to the crisis to ‘recovering’ in a world still plagued by the virus.

Carefully balancing the health risks with risks of the economic kind will be of paramount importance. It would appear that the path forward is one where economies reopen gradually, alongside actions to minimize health risks, including testing, surveying, and tracing. There is little doubt that reopening will likely lead to more cases. But, a gradual lifting of restrictions, so as to not overwhelm the health care system, should help reduce economic scarring that often results when the downturn lasts a long time.

Importantly, not all countries are yet able to reopen their economies and are unlikely to begin recovering for weeks or even months. There is also a real risk of additional domestic outbreaks this year or beyond. Moreover, differences between countries in access to resources, economic structure, and fiscal capacity foretells a global recovery that will be protracted and very uneven. Better buckle-up, since it may be a bumpy ride.

We also want to stress that economic statistics will look astonishing as the recovery takes hold, despite its protracted nature. To illustrate the issue we need to consider the arithmetic: recovering from a 5 percent decline requires a rebound of 5.2 percent, whereas rebounding from a 50 percent drop necessitates a surge of 100 percent! In light of the severity of the global and Canadian downturns, even strong recovery numbers will leave the level of activity depressed.

As an example, the results of the Labour Force Survey in May indicated the Canadian economy added 289 thousand jobs. In typical times, even a tenth of that is very strong. But, the number pales in comparison to the more than three million lost in the prior two months. In fact, the gain still left the unemployment rate (including workers not looking for work due to health risks) at close to 20 percent. So, despite the base case forecast looking strong and almost ‘V’-shaped, the severity of the drop in economic activity means that this recovery will look more like checkmark or swoosh—a steep decline followed by a slow return to the prior level.

When thinking about the downturn and the subsequent hoped-for recovery, particularly at the industry-level, we have considered a myriad of cyclical, structural, and even non-economic factors.

Where do we go from here?

What has become apparent is that the unprecedented shock that is the COVID-19 pandemic has initiated changes in a number of sectors. It has also become a catalyst for ongoing trends in several industries and the economy in aggregate. Let us take a moment to highlight some of the key considerations.

Canada’s population is aging rapidly and is increasingly reliant on immigration for growth. Moreover, older Canadians face greater health risks and their savings have been impacted by financial market volatility. COVID-19 may reduce their labour participation and their willingness to spend during the recovery and beyond.

Canada still remains open to immigration, but may not be able to attract as many newcomers given the increased health risks of international travel.

Canada is committed to addressing climate change. There is an opportunity for governments to use their COVID policy actions to accelerate the shift to a less carbon-intensive economy. The federal government program to address orphan wells in the energy sector is a case in point.

Businesses and governments have been forced to accelerate their shift to digital. This will impact business investment during the recovery, but the changes to business processes may temper the labour market recovery.

Organizations have been shifting to flexible workplaces and promoting remote work. For many, the imposition of containment rules has made remote work a necessity. There are many studies on the increased productivity from remote work, including the time saving on commuting, but the shift that took place by government edict has been abrupt. Many workers and businesses were not ready for working from home. This was made more difficult by school and daycare closures. As such, labour productivity may have been reduced. Worker preferences aside, businesses will want to see the return on their investment to deploy the remote-work infrastructure. Many will also recognize the potential cost savings from commercial real estate. This spells trouble for commercial real estate prices and may dampen commercial real estate construction.

Similarly, due to the need to maintain physical distancing, some firms are expanding the use of automation. This could help boost business investment during the recovery, but also impinge on labour demand.

The rise of protectionism has been affecting global supply chains for years. But, the pandemic has severely disrupted supply chains in ways firms and governments never contemplated. As the recovery unfolds, many global supply chains will be altered. For example, some businesses are thinking about supply chain redundancy in case of future disruption.

Governments have become aware that it may be necessary to have certain essential products produced domestically. Restoring essentials (medical supplies and equipment) or strategic products (electronics, defence) should help future investment. But, the need for uninterrupted supply will need to be balanced with the diminished gains from trade.

The role of government has been greatly expanded. Governments are now responsible for managing and ensuring business work environments, such as distance between the restaurant tables or the height of plexi-glass partitions. Through the Large Employer Financing Facility, the federal government is taking a stake in businesses that make use of the program, while restricting executive pay and share buy-backs.

Geopolitical risks have increased. The tragic health toll and economic hardship wrought by COVID-19 have motivated many countries to take a harder line with China. While this may subside once the pandemic is eradicated, it highlights increased political risk during the recovery. Conflict between China and the West was likely inevitable, but political risks during a slow economic recovery are a bad combination.

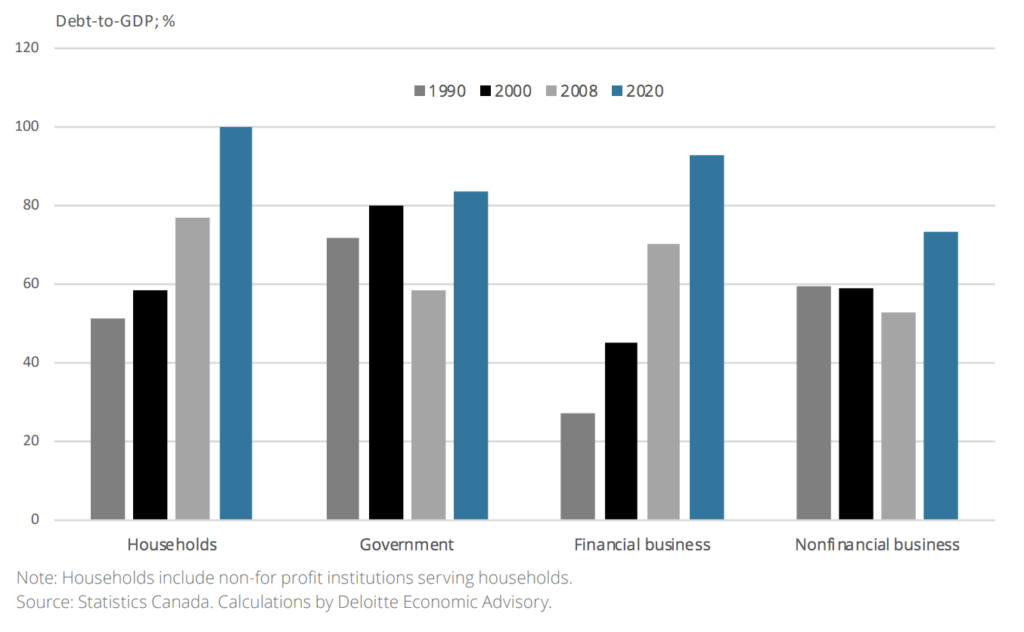

Debt-to-GDP; %

The key economic legacy of COVID-19 will be debt. Job losses and reduced hours have hit household incomes, making for highly indebted consumers—indeed, debt-to-income ratios are likely to rise substantially in Canada from already high levels (see Figure 2). Lower demand and additional costs of doing business will also indebt businesses. And, perhaps most dramatically, the cost of supporting workers and businesses during the downturn will leave governments laden with debt. The additional debt will likely temper the pace of recovery and leave economies ever more fragile going forward.

There may also be changes in how consumers behave during the recovery, particularly until a vaccine is deployed. Given the health risks, consumers are likely to make fewer trips to stores and be reluctant to touch products on shelves, make larger purchases per trip but in aggregate buy less.

The need for continued physical distancing will restrict how many customers can be present at stores, restaurants, and gyms. This will not only impact the volume of sales but will also limit the number of workers needed.

A key uncertainty is about how governments wind down the income and credit support programs put in place. For example, the CERB provides unemployed workers with $500 per week for up to six months. But, this program will eventually end. At that point, unemployed workers will need to be transferred onto Employment insurance support, but many workers do not qualify for EI. The government may launch an EI- equivalent program for those not eligible. But, these income-support programs are less generous that the CERB. Similarly, banks are offering mortgage deferrals for up to six months. That will help financially strained Canadians, but the deferrals will cease at some point. The implication is that we have only seen a portion of the income and unemployment shock. The same is true for business bankruptcies. In April, consumer and business insolvencies were lower than in March and down significantly from a year prior. However, this masks the true state of insolvencies, which are being delayed by the government in hopes of limiting them.

Finally, the Canadian recovery will also be shaped by the prospects for hard-hit industries. In many cases, the industries that are hardest hit will have the longest recovery. International tourism and air travel, for instance, will be severely restricted while the virus remains a concern. Retailers will have to adapt to even lower spending at brick-and-mortar stores going forward, while eating at home may become more frequent over dining out at restaurants (whether by preference or income constraints). The Canadian oil industry will continue to be challenged by excess supply and elevated inventory levels. Despite the likelihood of languishing prices, oil production will rise because of past investment and the prohibitive costs of restarting, but the impact on investment may never fully unwind.

Canadian outlook

When we consider all of the above, there is a strong case for a slow recovery.

Consumer spending accounts for nearly 60 percent of economic activity. Households may be cautious in their spending and the labour market recovery could take considerable time. This suggests only modest-to-moderate economic growth after the initial rebound from reopening.

Residential investment has thus far held its own during the lockdown, with new home construction particularly resilient. However, there is a real risk of a home price correction, with construction likely to follow. Higher unemployment, reduced personal income, continued health risks, and higher indebtedness are not positive for the real estate market. There is also a risk of a flood of condos held by investors onto the market as properties fail to provide adequate rental income. Commercial real estate (CRE) is especially vulnerable given the shift to remote work. Industrial and warehouse CRE will be less affected than retail or office CRE, but even with reshoring and e-commerce gains, it is unlikely to escape unharmed. Business investment will be constrained by financial losses, but essential investments in areas like digital and automation will continue.

Business investment should improve as firms address the heightened health risks and the economy recovers. But, as previously discussed, sectors such as energy will buck this trend.

Capital expenditures by the federal and provincial governments should be boosted by stimulus measures yet to be announced. Governments often prioritize infrastructure investment for stimulus since they have a high economic multiplier. We expect that instead of the typical roads and bridges, governments will choose to focus on digital, health care, and education.

Government spending will be solid in the near-term, but will likely be constrained as the recovery strengthens and governments start thinking about fiscal rebalancing. Realistically, this is a longer-term theme, unlikely to be undertaken before 2022 at the earliest.

Canadian international trade should recover alongside the global economy. Exports should also benefit from a US recovery and the possibility that some firms bnear-shore activities to North America. And, while the energy sector is expected to lag, it should benefit from the global recovery and less disagreement among OPEC+ members.

Given the massive fiscal and monetary stimulus, some worry about an acceleration in inflation. At the moment, inflation risks are low. In fact, risks of deflation are far more concerning given the magnitude of the recession. Inflation could rise if the amount of fiscal and monetary policy stimulus is not reduced once the economy is back on its feet. However, this is unlikely given the temporary nature of fiscal measures.

Here are few numbers

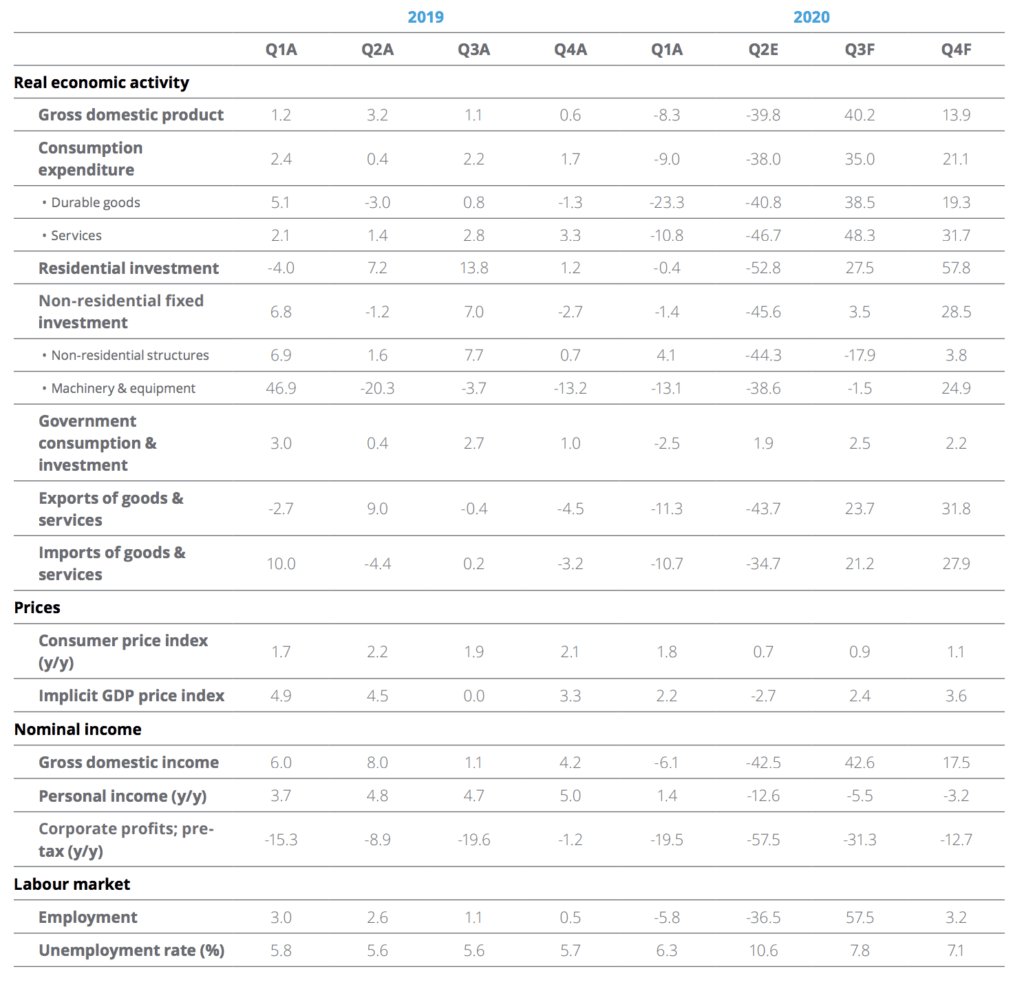

So, putting all of the elements together, what is the outlook for Canadian economic growth? After contracting by an annualized 8.3 percent in the first quarter of 2020, the economy is estimated to have plunged 39.8 percent in the second quarter. However, growth looks to have resumed in May, with the economy expected to grow by an average of 27 percent annualized in the second half of the year. For the year as a whole, the Canadian economy is slated to contract by 5.9 percent, before rebounding by 5.6 percent in 2021.

Canadian employment will drop 3.5 percent this year before rising 3.7 percent next year. While this may sound strong, the unemployment rate at the end of 2021 will still be well above pre-COVID-19 levels.

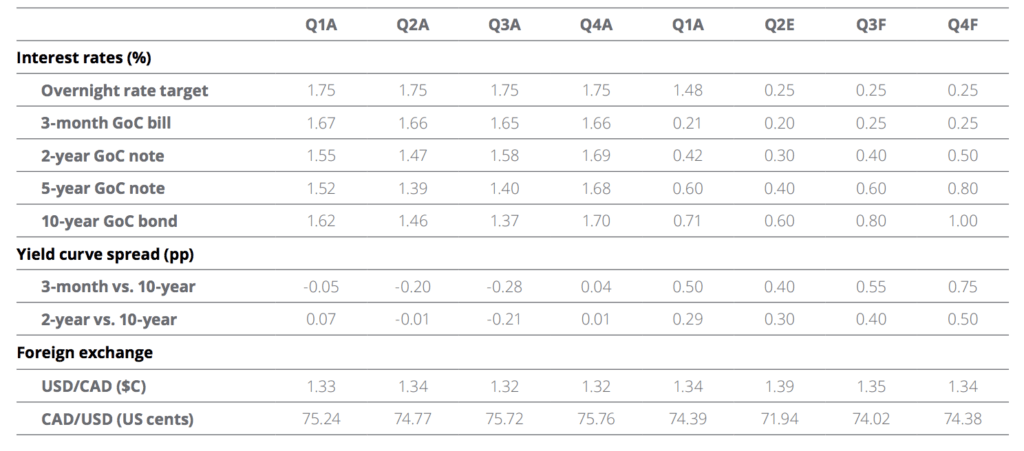

Reflecting the gradual recovery, the Bank of Canada is expect to keep interest rates at current levels until at least late 2021.

The Canadian dollar weakened earlier this year in reaction to declining commodity prices, diminishing economic prospects, and safe-haven buying of US dollar assets by investors. As the economic risks diminished and commodity prices stabilized, the Canadian dollar has rebounded to near 74 US cents at the time of writing this report. Looking ahead, we expect the loonie to rise slightly from current levels.

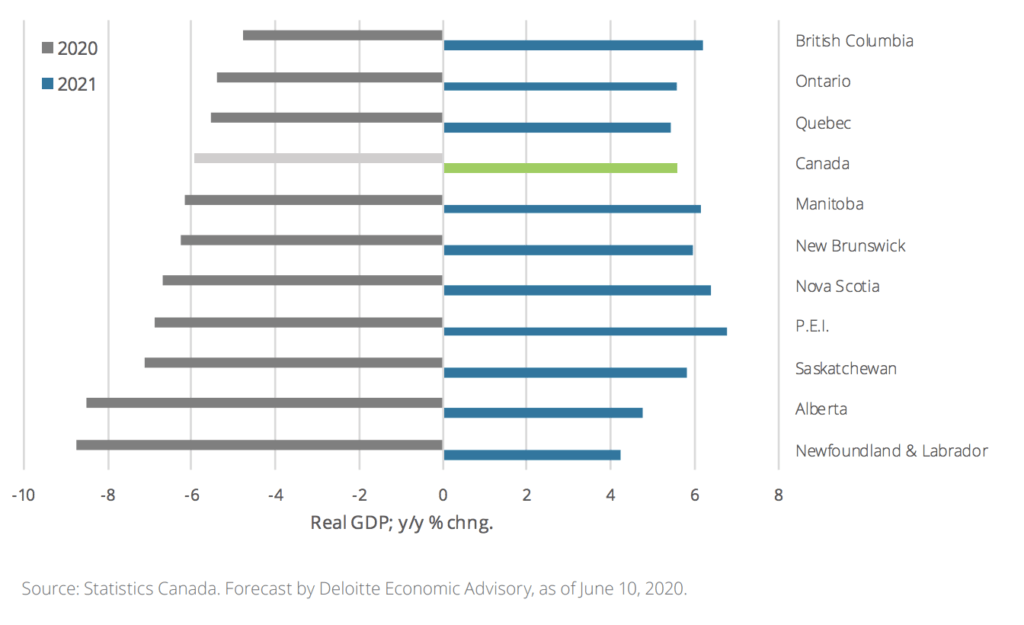

Provincial outlook

The Alberta and Newfoundland and Labrador economies will experience the most severe contractions in 2020, with real GDP falling by well above 8 percent, while Saskatchewan will see a contraction of near 7 percent. This poor performance reflects their high energy sector concentration.

The remainder of the Maritimes and Manitoba will decline by slightly more than the national average, while the central provinces of Ontario and Quebec will fare slightly better than the national average.

Lastly, the BC economy will be the outperformer, posting the mildest downturn and returning to pre-COVID levels the quickest. As for the recovery, gains in 2021 will be spread across all provinces, but the hardest hit will tend to be the slowest to recover.

Figure 3: Provincial forecast

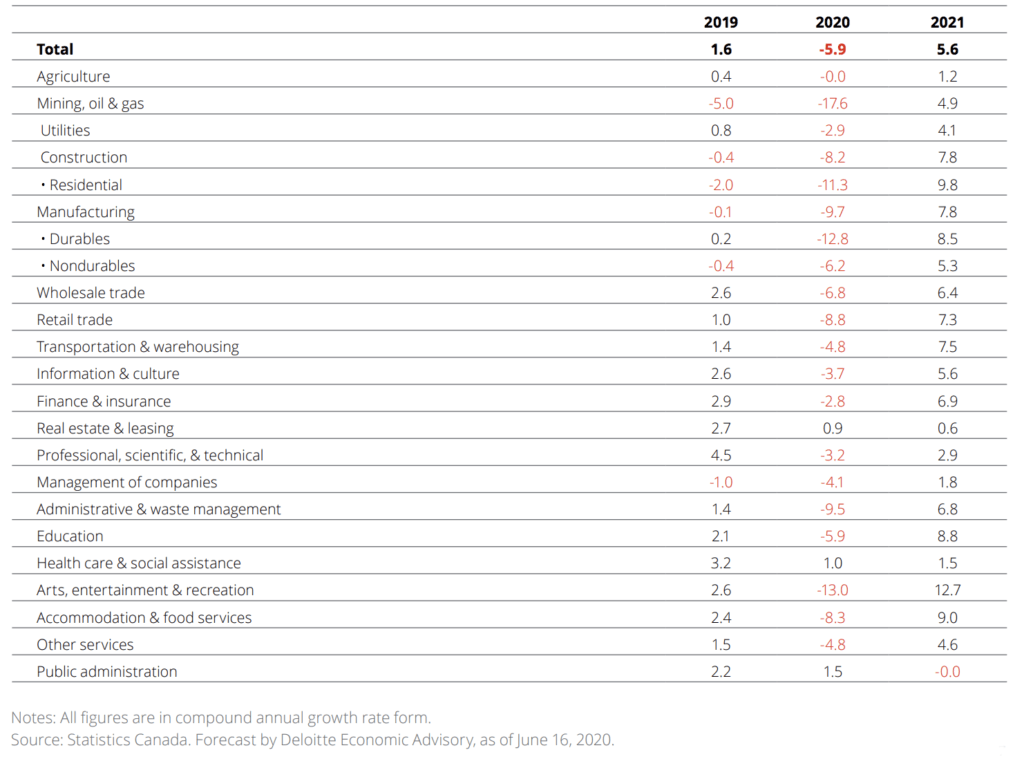

Industry outlook

The hardest hit industries include mining, oil and gas, entertainment and recreation, and durables manufacturing (such as autos).

All the above-mentionned sectors are expected to see double-digit contractions. Other industries that will be hard hit include retail, transportation, administrative services, accommodation, and food services.

Professional and financial services will see the mildest declines, given the ease of remote work. Lastly, two industries should post growth this year, with activity rising in health care and public administration tied to the fight against COVID-19.

The attached industry forecast table provides details of the downturn and recovery by economic sector.

Industry GDP forecast

Canada: Economic forecast

Canada: Financial forecast

Concluding remarks

The Canadian economy will suffer a deep recession this year, but the tide is already turning.

The key risk is a second round of infection, particularly if it leads to renewed lockdowns. So long as this does not occur, and the gradual reopening continues globally, a recovery should unfold in Canada in the second half of 2020.

However, the road to a full recovery, defined as economic activity reaching its pre- COVID-19 level, will take at least six quarters. This is due to continued health risks and the gradual nature of the economic reopening. It will also be hindered by expected weakness in the commodity sector.

The pandemic, lockdown, and reopening are fueling many trends that will not only shape the recovery, but will also affect the performance of Canadian industries. The recession will also leave behind deep and transformative legacies. For example, the additional government debt will be with us for years to come. But, it was the price to avoid a depression. The shift to digital, AI and automation, and remote work can be productivity enhancing, but may also have labour market consequences sooner than was anticipated.

Make no mistake, the fallout of the COVID-19 pandemic has been unprecedented in many ways. It is becoming increasingly apparent that its legacies may be unprecedented, or at least long lasting, too.

Moving the needle forward on becoming financially independent doesn’t mean doing all of these tips, although why not try adopting 1 or 2 each month. From the best ways to budget to how to boost your earning potential like a pro, these tips of financial wisdom are sure to get you headed in the right direction.

First Things First: A Few Financial Basics

1. Create a Financial Calendar

If you don’t trust yourself to remember to pay your quarterly taxes or periodically pull a credit report, think about setting appointment reminders for these important money to-dos in the same way that you would an annual doctor’s visit or car tune-up.

✅ TIP: Consider making a list of your bills and due dates. Leave it out where you see it every day and make a note of when and how much you paid towards the bill. Visually you will see which bills you forgot to pay this month. To keep a good credit score, don’t miss paying at least the minimum due each month.

~ David Aaron, Aaron Wealth Management

2. Check Your Interest Rate

Q: Which loan should you pay off first? A: The one with the highest interest rate. Q: Which savings account should you open? A: The one with the best interest rate. Q: Why does credit card debt give us such a headache? A: Blame it on the compound interest rate. The bottom line here: Paying attention to interest rates will help inform which debt or savings commitments you should focus on.

3. Track Your Net Worth

Your net worth—the difference between your assets and debt—is the big-picture number that can tell you where you stand financially. Keep an eye on it, and it can help keep you apprised of the progress you’re making toward your financial goals—or warn you if you’re backsliding.

How to Budget Like a Pro

4. Set a Budget, Period

This is the starting point for every other goal in your life. Debt can creep up on you. It’s so easy to accept small financial obligations in today’s society with smartphones. Some of those apps on your phone are free while others have a small monthly fee. Netflix’s basic plan is only $10 per month, so are many other fun and useful apps. Next thing you know you’re into hundreds of dollars in monthly obligations.

✅ TIP: Consider looking at your life as a business or corporation. You can only spend what you earn and you also need to conserve cash for future growth and for rainy days.

~ David Aaron, Aaron Wealth Management

5. Consider an All-Cash Diet

If you’re consistently overspending, this will break you out of that rut. Now, this is a little harder to do given many companies want a credit card just to open an account. Try renting a car without a credit card for example. The benefit of paying cash for as many things as possible is being hyper-aware of what you’re spending your money on.

6. End of day money review

At the end of your day take a couple of minutes to review what you spent money on (Hopefully one bill was a deposit to your savings). This reflection helps to identify problems or negative patterns immediately and keeps track of goal progress.

✅ TIP: You make XX amount of money each year. The moment you buy something you’ve given up that money. It’s gone forever. Ask yourself this question: How does this purchase add value to my life?

~ David Aaron, Aaron Wealth Management

How to Get Money Motivated

7. Create a Financial Vision Board

You need the motivation to start adopting better money habits, and if you craft a vision board, it can help remind you to stay on track with your financial goals. More than that it’s a psychological trick ( a healthy one). Your subconscious mind will work day and night (that’s right, even when your sleeping) to bring these images into reality.

8. Set Specific Financial Goals

Use numbers and dates, not just words, to describe what you want to accomplish with your money. How much debt do you want to pay off—and when? How much do you want saved, and by what date? Napoleon Hill’s book “Think & Grow Rich” has a chapter which in my opinion is one of the best step-by-step processes to helping you achieve any goal, especially financial goals.

9. Make Bite-Size Money Goals

One study showed that the farther away a goal seems, and the less sure we are about when it will happen, the more likely we are to give up. So in addition to focusing on big goals (such as, buying a home), aim to also set smaller, short-term goals along the way that will reap quicker results—like saving some money each week in order to take a trip in six months.

1o. Banish Toxic Money Thoughts

This has everything to do with your internal dialog and how you view money. Negative thoughts and spoken words have power. Cut them off right in there tracks.

✅ TIP: Be mindful of your thoughts and choose your words carefully. Karma is the energy created by thoughts and words. Careless thoughts & words will produce negative energy. Good thoughts & words produce good energy. If you want good things to show up in your life, cut out your negative thoughts & words.

~ David Aaron, Aaron Wealth Management

11. Get Your Finances–and Body—in Shape

One study showed that more exercise leads to higher pay because you tend to be more productive after you’ve worked up a sweat. So taking up running may help amp up your financial game. Plus, all the habits and discipline associated with exercising are also associated with managing your money well.

12. Appreciate what you have

Do you have clothes hanging in your closet with tags still on them? Maybe it was an impulsive purchase or you couldn’t pass up a sale. Being content with what you already have is not only a healthy state of mind, it will also slow your impulsive spending.

How to Amp Up Your Earning Potential

13. When Negotiating a Salary, Get the Company to Name Figures First

If you give away your current pay from the get-go, you have no way to know if you’re lowballing or highballing. Getting a potential employer to name the figure first means you can then push them higher.

14. You Can Negotiate More Than Just Your Salary

Your work hours, official title, maternity and paternity leave, vacation time, and which projects you’ll work on could all be things that a future employer may be willing to negotiate. Employers have learned lessons from COVID-19 and are more inclined to have employees work from home. This is a huge saving for employees in areas such as; transportation, dining out, work clothes, and even time. Yes, time is money.

15. Make Salary Discussions at Your Current Job About Your Company’s Needs

Your employer doesn’t care whether you want more money for a bigger house—it cares about keeping a good employee. So when negotiating pay or asking for a raise, emphasize the incredible value you bring to the company.

How to Keep Debt at Bay

16. Start With Small Debts to Help You Conquer the Big Ones

If you have a mountain of debt, studies show paying off the little debts can give you the confidence to tackle the larger ones. You know, like paying off a modest balance on a department store card before getting to the card with the bigger balance. Of course, we generally recommend chipping away at the card with the highest interest rate, but sometimes psyching yourself up is worth it.

17. Don’t buy too much house

This happens when you fall in love with a house where your mortgage is near 30% of your take-home pay. You’re going to curse that house you fell in love with when your not able to enjoy living because you have no money left.

How to Shop Smart

18. Evaluate Purchases by Cost Per Use

It may seem more financially responsible to buy a trendy $5 shirt than a basic $30 shirt—but only if you ignore the quality factor! When deciding if the latest tech toy, kitchen gadget, or apparel item is worth it, factor in how many times you’ll use it or wear it. For that matter, you can even consider cost per hour for experiences!

A good example of this is your bedroom. You’re going to spend about a third of your life in bed and getting a great sleep is immeasurable. We waited for the bedroom set we loved to go 50% off. It cost us $13,000 and we kept it for 14 years. Sounds crazy to calculate this but…it cost us $2.55 to sleep each night over those 14 years!

19. Spend on Experiences, Not Things

Putting your money toward purchases like a concert or a picnic in the park—instead of spending it on pricey material objects—gives you more happiness for your buck.

20. Go shopping by yourself

Ever have a friend declare, “That’s so cute on you! You have to get it!” for everything you try on? Save your socializing for a walk in the park, instead of a stroll through the mall, and treat shopping with serious attention.

How to Save Right for Retirement

21. Start Saving NOW!

Not next week. Not when you get a raise. Not next year. Today. Because the money you put in your retirement fund now will have more time to grow through the power of compound growth. Albert Einstein said, “Compound Interest is man’s greatest invention.”

22. Do Everything Possible Not to Cash Out Your Retirement Account Early

Dipping into your retirement funds early will hurt you many times over. For starters, you’re negating all the hard work you’ve done so far saving—and you’re preventing that money from being invested. Second, you’ll be penalized for an early withdrawal, and those penalties are usually pretty hefty. Finally, you’ll get hit with a tax bill for the money you withdraw. All these factors make cashing out early a very last resort.

22. Get that free cash

Take advantage of your employer’s group retirement plan as many plans match your contribution (to a maxed percentage). But you’ll only get that contribution if you contribute first. Another hidden advantage is the fee for investing. Group plans tend to have very low investment fund fees (under 1%). To get these low fees outside your group plan you would either need a lot of money to qualify for a lower fund fee or invest in index funds & Exchange Traded Funds (ETF). A group plan solves that issue for you.

23. When You Get a Raise, Raise Your Retirement Savings, Too

You know how you’ve always told yourself you would save more when you have more? We’re calling you out on that. Every time you get a bump in pay, the first thing you should do is up your automatic transfer to savings, and increase your retirement contributions. It’s just one step in our checklist for starting to save for retirement.

Building credit

24. Review Your Credit Report Regularly—and Keep an Eye on Your Credit Score

This woman learned the hard way that a less-than-stellar credit score has the potential to cost you thousands. She only checked her credit report, which seemed fine—but didn’t get her actual credit score, which told a different story.

25. Keep Your Credit Use Below 30% of Your Total Available Credit

Otherwise known as your credit utilization rate, you calculate it by dividing the total amount on all of your credit cards by your total available credit. And if you’re using more than 30% of your available credit, it can ding your credit score. If your interested in having the best score keep your utilization rate below 10%.

26. If You Have Bad Credit, Get a Secured Credit Card

A secured card helps build credit like a regular card—but it won’t let you overspend. And you don’t need good credit to get one!

How to Get Properly Insured

27. Get More Life Insurance on Top of Your Company’s Policy

That’s because the basic policy from your employer is often far too little and if you get fired so too is your life insurance. There are usually provisions to continue your insurance although the price is not as competitive as getting your own. Life insurance will never be cheaper than it is today. Sounds like a sales phrase but seriously, it’s based on your age & health. It gets more expensive for you to buy as you age so lock in those premiums now.

28. Get Renters Insurance

It, of course, covers robberies, vandalism, and natural disasters, but it could also cover things like the medical bills of people who get hurt at your place, damages you cause at someone else’s home, rent if you have to stay somewhere else because of damage done to your apartment—and even stuff stolen from a storage unit. Not bad for about $30 a month!

Be Prepared for Rainy (Financial) Days

29. Make Savings Part of Your Monthly Budget

If you wait to put money aside for when you consistently have enough of a cash cushion available at the end of the month, you’ll never have money to put aside! Instead, bake monthly savings into your budget now.

30. Keep Your Savings Out of Your Checking Account

Here’s a universal truth: If you see you have money in your checking account, you will spend it. Period. The fast track to building up savings starts with opening a separate savings account, so it’s less possible to accidentally spend your vacation money on another late-night online shopping spree.

✅ TIP: Grant Cardone says, “Get Broke each month. Get rid of your savings. You can’t save your way to being wealthy. You need to get it invested as quickly as possible.”

Why, you ask? Because it makes you feel like the money you shuttle to your savings every month appears out of thin air—even though you know full well it comes from your paycheck. If the money you allot toward savings never lands in your checking account, you probably won’t miss it—and may even be pleasantly surprised by how much your account grows over time.

32. Consider Switching to a Credit Union

Credit unions aren’t right for everyone, but they could be the place to go for better customer service, kinder loans, and better interest rates on your savings accounts.

33. There Are 5 Types of Financial Emergencies

Hint: A wedding isn’t one of them. Only dip into your emergency savings account if you’ve lost your job, you have a medical emergency, your car breaks down, you have emergency home expenses (like a leaky roof), or you need to travel to a funeral. Otherwise, if you can’t afford it, just say no.

34. Have 6 months of emergency cash

Rule #1. Pay Yourself First! Start saving right away into an account where this money will only be used in the case of an emergency as mentioned above. There are many opinions on the amount, although 6 months of expenses is appropriate.

How to Approach Investing

35. Pay Attention to Fees

The fees you pay in your funds, also called Management Expense Ratios (MER), can eat into your returns. Even something as seemingly low as a 1% fee will cost you in the long run. Index funds & Exchange Traded Funds (ETF) are the lowest fees on the market although bear in mind getting advice may be challenging as fees are used to pay for the advice. A low fee may mean no advice.

36. Rebalance Your Portfolio Once a Year

If you’re not getting advice from an advisor then you will need to do this yourself. I strongly recommend you use an advisor, studies show investment accounts with an advisor are higher as compared to no advice. What does Rebalancing mean? Let’s say you had allocated your portfolio to have 60% equities & 40% bonds. Throughout the year these values change because of gains or losses in your investments. At the start of the year, rebalance your portfolio to ensure you still have a 60/40 split.

Get the benefit of experience and knowledge from a team of seasoned professionals who can assess your needs and suggest appropriate strategies. Simply saving money isn’t enough – creating a financial plan with the help of professionals will help you achieve your goals much faster.

Why should I have so much insurance, it’s not like I’m going to use the money?

That’s what many middle-class Canadians say about insurance, although wealthy families have an entirely different view of insurance (especially the ones who stand lose a huge chunk of their wealth to taxes). But the truth is that many taxes and related expenses – whether on investment income, capital gains, or on death – can be legally avoided now with proper planning.

Insurance can be the most versatile and reliable financial product in your portfolio. Many Canadians don’t know how to use it to preserve their hard-earned money and achieve desirable tax outcomes. Nor do they know that it’s available to everyone. When we think of insurance, many people think it’s used for burial expenses and to leave a little money behind. It also happens to be the greatest wealth-building tool available to everyone.

Life Insurance enjoys unique treatment under our Income Tax Act. Consider using it to reduce or eliminate your taxes, leaving more tax-free funds to family and favourite charities. Health and disability insurance will protect your earnings if you get sick and provide access to the finest medical care in the world, while property and casualty insurance products protect your business, home and tangible assets.

In fact, there has never been such a good time to buy insurance. Here are 10 ways to use insurance to increase your wealth.

1. Life Insurance as a Wealth Building tool

If you are like every person I meet, you want to leave as much as possible for your family (and hopefully your favourite charity) and as little as possible – ideally nothing – to the government. Canadians who die without a spouse or financially dependent child or grandchild, unwittingly leave the government up to half of the value of their Registered Retirement Savings Plans and Registered Retirement Income Funds.

A further tax of 25 per cent is payable on the growth of your non-registered holdings like real estate and bonds. And there are still estate costs that have to be paid.

Life insurance can mitigate those losses by providing tax-free funds to the estate and its beneficiaries.

2. Estate preservation

The main goal of estate preservation is to minimize the tax burden at death.

To do this properly, start by developing a robust financial plan with your financial advisor, who will ask you what you want to do in retirement and where you want your money to go after you die.

If you own shares in a private holding company or investment corporation, proper planning now can reduce or eliminate the double taxation that will result from the deemed disposition of the shares at death and the tax liability on the final distribution of the assets out of the corporation.

The last thing you want is having to sell an asset to pay the tax liability at death.

~ David Aaron, Aaron Wealth Management

3. Wealth Transfer

While many people believe they can only buy life insurance for themselves or as part of a joint last-to-die policy, it’s also possible to transfer wealth by buying a life insurance policy on a child or grandchild.

As the owner of the policy, you pay the premiums, and if you pay more than what is needed you create cash value. When the policy is transferred to the child in the future it may qualify as a tax-free rollover and the child will have access to the cash value. If you transfer the policy to the child once he/she is 18 and there is a policy gain, that income is attributed to the child, not you (It also happens to be a legal method of avoiding taxation on the growth of your investment).

4. Immediate Financing Arrangement (IFA)

A leveraging strategy can allow you to obtain a life insurance policy without having to use your own funds to pay the premium. You can enjoy all of the tax benefits and vastly increase the value of your estate while your own money continues working for you in your business or investment portfolio.

IFA policyholders pay only the interest cost on the borrowed premiums for a permanent or whole life insurance policy. The loan gets paid off from the ultimate death benefit payout. Along the way, all of the interest paid is tax-deductible and the tax savings can be used to reduce the outstanding balance on the line of credit. The after-tax interest cost on a $100,000 insurance premium is usually just a few thousand dollars in the current rate environment.

5. Is your will up to date?

While insurance can go far in helping to preserve your estate, all will be for naught if you don’t have a will. More than half of Canadians do not have an up-to-date will.

Your will is the very heart of estate preservation, ensuring that your assets will go to your heirs or a charity beneficiary according to your wishes.

Without a will, your estate will be administered by a bureaucrat according to applicable provincial law. Most provinces grant a preferential share of the estate to the spouse and the rest gets split between the spouse and children.

Certain assets, like private company shares, don’t have to go through probate and should be dealt with in a secondary will.

6. Disability Insurance

Successful Canadians who check the fine print of their company benefits booklet are usually surprised to learn that while they enjoy a healthy annual compensation package, their long-term disability coverage is insufficient and may only pay out to a maximum of $10,000 a month, all of it fully taxable.

High-limit disability insurance is now available with coverage of up to $150,000 a month or $2 million per year, all non-taxable.

7. Long-Term Care Insurance and Critical Illness Insurance

The biggest and fastest growing demographic in Canada – and most of the world – is seniors. Statistics Canada predicts more than seven million seniors by 2021.

Long-term care facilities now cost about $4,000-$10,000 a month and can rapidly deplete retirement savings, putting a financial strain on a spouse or family.

Recognizing that the cost of long-term care or suffering a critical illness can be significant, wealthy people buy policies that include a return of premium option, and if no claim is made they get back all of the premiums paid.

You can also purchase joint last-to-die insurance that will enable you to enjoy your retirement years without worrying that you won’t be able to leave something for children or a favourite charity.

8. Best Doctors Insurance®

We live in a great country, with a health care system that provides universal coverage (and long wait times for treatment) through our taxes. But all those taxes aren’t enough to get you the specialized care you need as quickly as you want it.

Best Doctors Insurance® provides immediate access to the finest healthcare at Centres of Excellence around the world with a $5 million lifetime fund to cover treatment costs.

A “healthcare concierge” helps you navigate the system, from diagnosis to treatment and recovery, and looks after everything from scheduling doctor’s appointments to arranging travel and accommodation. No doctor’s referral note is required.

Service providers are paid directly (it’s not a reimbursement plan) for tests, procedures, treatments and surgeries not available in Canada.

9. Leave a Legacy

Many people have a favourite charitable organization near and dear to their hearts, whether it’s an organization devoted to an illness that afflicted a family member or a school that helped them get to where they are today

As a parent/grandparent/great-grandparent, you can set up a strategy that will provide ongoing giving through an endowment in the form of an irrevocable gift to a private foundation or a donor-advised fund (DAF) within a public foundation.

A DAF requires that a board of directors be set up to distribute the funds. Often adult children or grandchildren join the board to keep their family’s name alive and be aligned with a specific cause.

If the decision is taken to provide for a charity through life insurance the proceeds are usually many times greater than the policy premiums and the family name will be remembered as a generous one that gives back to the community. It’s also a great way to instill a love of philanthropy in the family, especially by having young family members involved in the process.

10. Property and casualty insurance

Above and beyond customary property and casualty insurance like house and car coverage, other aspects of your life deserve appropriate protection.

Your office is your second home and should have coverage that includes potentially costly flood damage and business interruption insurance. The latter compensates for lost income resulting from catastrophes like a major weather event (ice or snow storm) that prevents you and your staff from going into the office.

Directors and Officers insurance protects you from lawsuits brought by investors, employees or customers. This insurance will pay for legal fees, settlements and other costs. Professionals like doctors, engineers and architects also need Errors and Omissions coverage in the event of a suit for errors or negligence.

Don’t go it alone. Get the benefit of experience and knowledge from a team of seasoned insurance professionals who can assess your needs and suggest appropriate strategies. Simply getting insurance in place isn’t enough – get the right types of insurance in the right amounts, with the help of professionals who will be there to advocate for you in the event a claim is made.

Besides loving education, summers off (for those of you not teaching summer school) above-average income (average Canadian employment income according to StatsCan age 45-54 is $64,800; age 35-44 was $59,600) plus benefits, teachers will receive a great pension.

The Ontario Teachers’ Pension Plan provides a pension income example: If you earn $85,000 in your five highest salary years and have 30 years of credit, your basic annual pension would be 2% × 30 × $85,000 = $51,000.

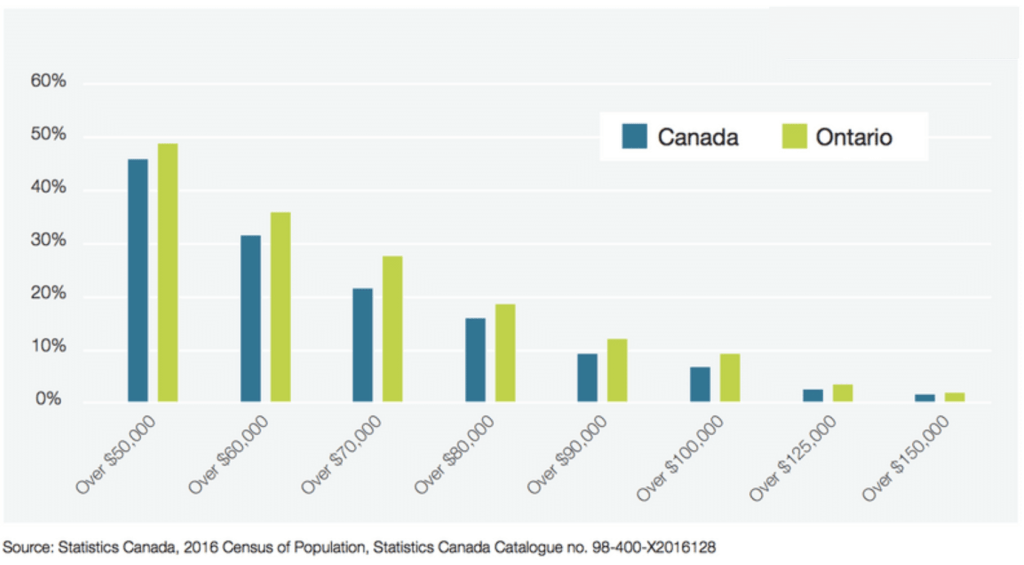

According to StatsCan, a retired couple had annual expenses between $40,800 to $48,600. Approximately 50% of retired couples have a combined total after-tax income greater than $50,000.

Couple: Cumulative after-tax income

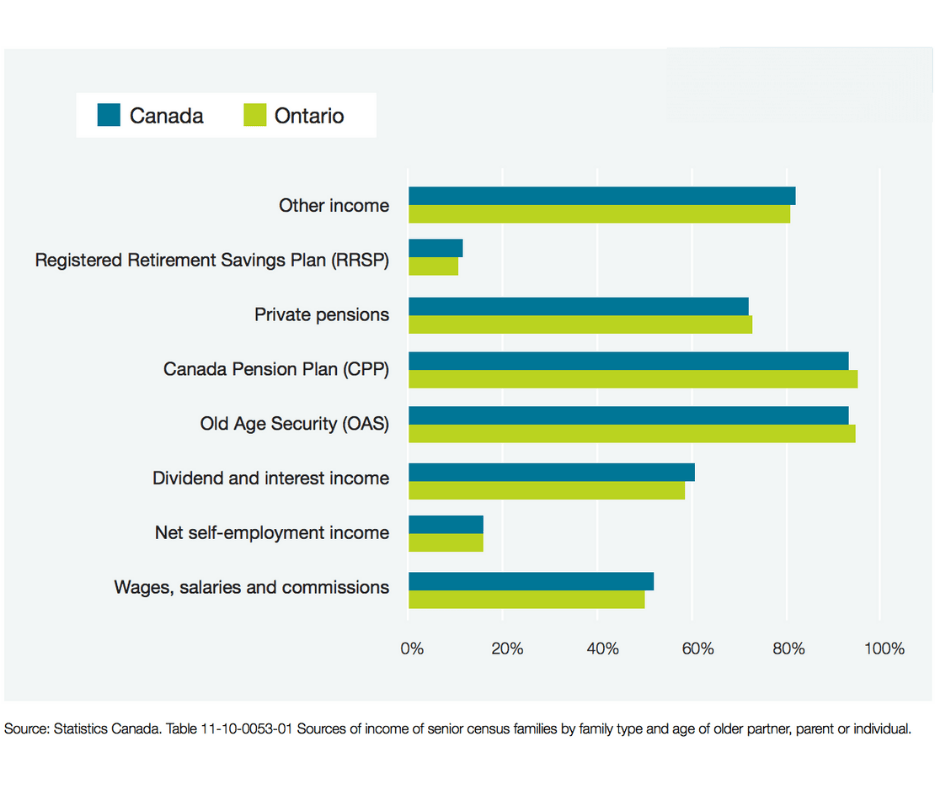

Sources of Income

When teachers marry teachers

When teachers marry another teacher and work as a teacher until they retire, their combined retirement income will provide income well above their living expenses (assuming they don’t try to live like the Kardasians). They will have roughly $30,000 of additional after-tax disposable income to spend any way they want. The #1 concern people have about retirement is: Will I have enough money to retire? When a teacher marries a teacher, they will not have that concern.

When you pray for rain you have to deal with the mud

Two married teachers really need a financial advisor because they already have their retirement income goal solved. The issue is where do you invest the excess cash you have throughout your retirement years? An RRSP will only create a larger taxable income for you. You’re also going to lose about 35% to taxes at the last death of the couple. What you need is a pool of money that will provide a non-taxable income stream at retirement (if you need it).

The #1 Wealth Building Strategy for Teachers

What if I told you, that you could invest into something that is boring, returned 5-6% per year with no tax, low risk, and if you died would pay your spouse more than 10x what you invested tax-free! How much money would you invest? Sounds too good to be true although this is the one exception that breaks the rule.

It’s Participating Life insurance. There are many advisors who will suggest using Universal life insurance however this should be avoided if using this strategy for wealth building. It may be the only type of permanent insurance the advisor sells, so ask questions.

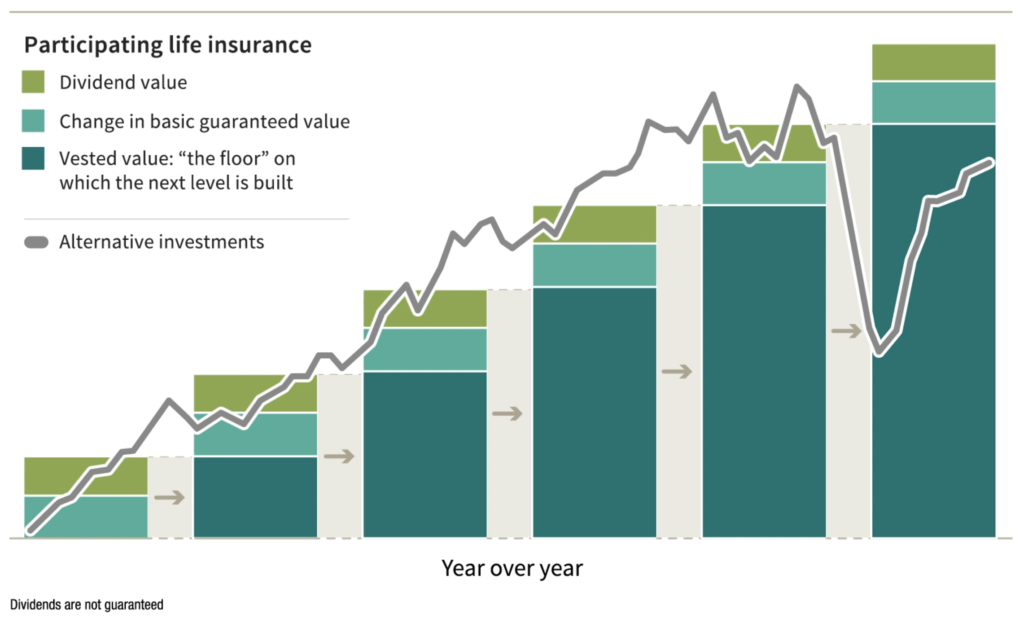

The advantage of participating life insurance is the accumulated cash value in your policy. When the annual dividend is deposited to your policy, it is reinvested into the fund producing compound returns, and because of the nature of how insurance cash values are invested your balance never decreases unlike investing in an RRSP. The illustration below compares the year over a year difference between accumulating cash values vs. the stock market. Note the far right column with a severe market decline (due to Corona Virus). The growth in the insurance cash value was unaffected and continued to grow.

In this strategy, you would deposit money to the insurance policy the same way you would if you were investing in an RRSP. The excess cash above the actual cost of insurance is invested in a fund managed by the insurance company (the fund is actually huge, about $41 billion). Because the money is used to pay death claims & dividends, the investment allocation has to be conservative. You’ll find about 20% of the fund is invested in the stock market and the rest are bonds, mortgages & private placement. The fund is largely unaffected by severe downturns in the stock market.

Not all investments are equal

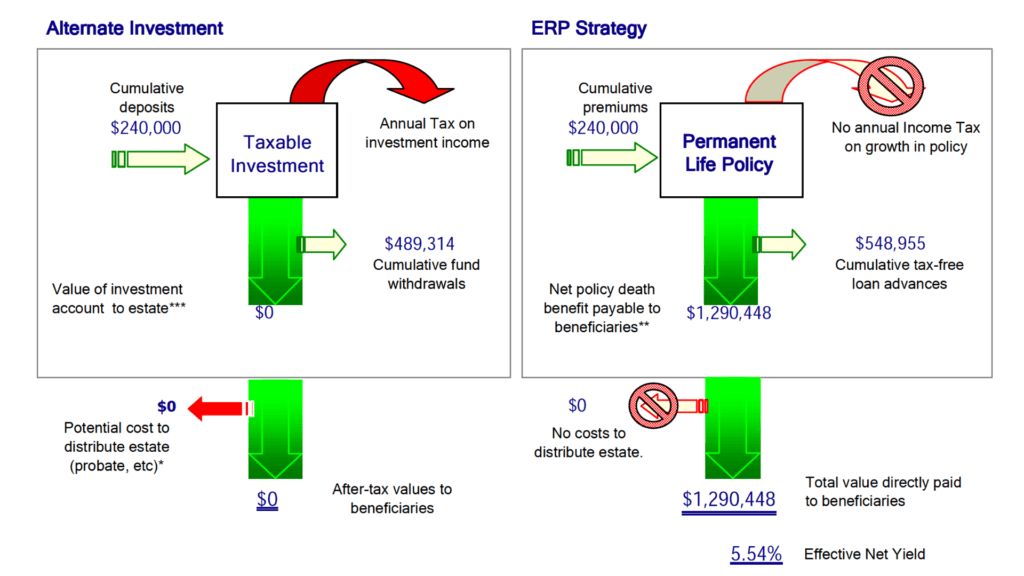

The illustration above compares a non-registered investment vs the participating life insurance. In this example on the left, we are depositing $1,000 per month for 20 years. In the mutual fund, $240,000 is invested and grows at 7% but is taxed each year. Annual taxation on the fund is a drain upon the longevity of the use of funds. A total of $489,314 is withdrawn over retirement. The owner passes away and there is No money left to pass to his/her heirs.

In the insurance example on the right, the same amount of money is invested, $1,000 per month for 20 years for a total of $240,000. There is no tax on the growth of the cash value which is one of the main advantages of participating life insurance. Over the course of retirement, the owner withdraws $548,955 ($59,641 more than the mutual fund) and the owner passes away at the same age as the mutual fund example. At his/her passing, $1,290,448 goes to his/her beneficiaries tax-free!

Clearly, the life insurance investment a superior wealth building solution as compared to an RRSP.

Additional advantages

Two teachers with pension income and RRSPs accounts will likely experience a claw-back of their government retirement income whereas, the income received from the life insurance is tax-free and will not affect their government retirement income.