Living Through Coronavirus

“Most people who fall sick with COVID-19 will experience mild to moderate symptoms and recover without special treatment” ~ who.in

In January 2020 we heard a virus was emerging from China and soon after people tested positive for Covid-19 also known as Coronavirus. In fact, the first presumptive case reported in Ontario (and Canada) was a man in his 50s, who came from Wuhan, China and begins self-isolating. His wife becomes the second case and begins self-isolating the following day. The man’s illness is officially confirmed two days later.

On February 26, Ontario had 5 confirmed cases of the Coronavirus and people appeared to be unconcerned. We were told to wash our hands frequently, that the seasonal flu virus affected more people each year.

Until this point, most people had a growing concern of the Coronavirus but not panicked until… March 12, 2020, when Doug Ford, Ontario’s premier announced that publicly funded schools across the province will be closed for two weeks following March break. While announcing the decision, the Ontario premier also tells families to:

travel and have fun

~Premier Doug Ford

When you’re told “have fun” nothing to worry about here, oh and by the way, we’re closing school for 2 weeks, that’s code for “full-blown pandemonium!” I was immediately reminded of the nuclear bomb drills we did at school as a child. Absolute panic and fear of what was to come.

Do you remember in March the frantic race to the grocery store, not to purchase Vitamin C but rolls and rolls of toilet paper. People’s greatest fear was not getting sick but not being able to wipe their butts! Seriously, people waited 2 hours in line to pay $40 for 12 rolls of toilet paper. Stockpiling toilet paper, Kleenex, baby wipes & sanitizers.

People began saying “stock up on everything. It’s going to be bad, they’re going to close everything.” It was Friday, March 13 my wife and I were grocery shopping as we do every Friday. While I’m not deeply superstitious, it was “Friday the 13th” after all. The grocery store is usually buzzing on Friday but this was crazy!

There was no meat as you can see and yes no toilet paper or sanitizer anywhere. From this moment on we lived in a different world. This was straight out of a science fiction movie.

Restrictions followed with businesses being closed, wearing a face mask, sanitizing your hands and, working from home. The government issued economic relief cheques to those who qualified and a huge swath of people were unqualified.

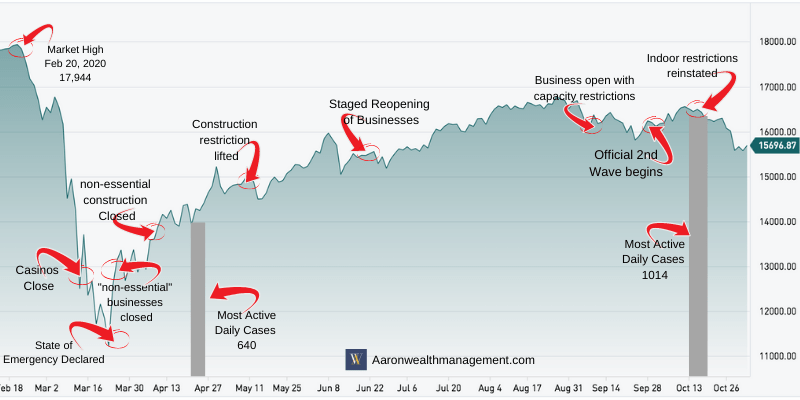

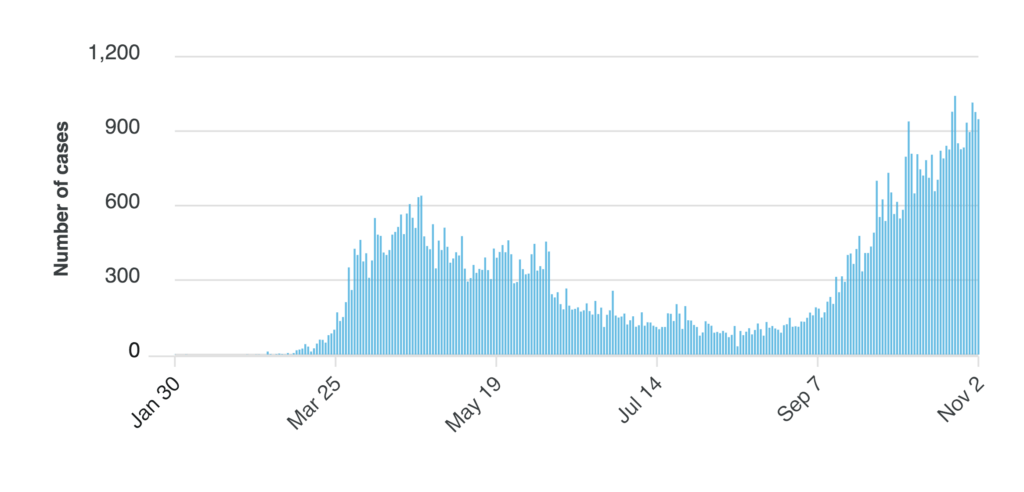

The peak of confirmed active daily cases of Covid-19 in Ontario was on April 23/24 with 640 infected people. Contrast that to the highest number of daily confirmed cases of 1,015 on October 15, 2020.

The difference between March and November is we really didn’t know what we were facing and how to deal with Coronavirus. We didn’t know anything about it and in fact the WHO’s direction on what to do changed several times. I’m not placing blame on anyone. We forget these are very difficult things to figure out and in fairness to the doctors and scientists, a great many people had to get sick first in order to determine how it attacks the body.

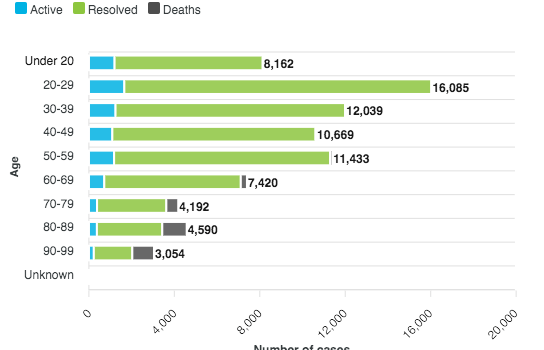

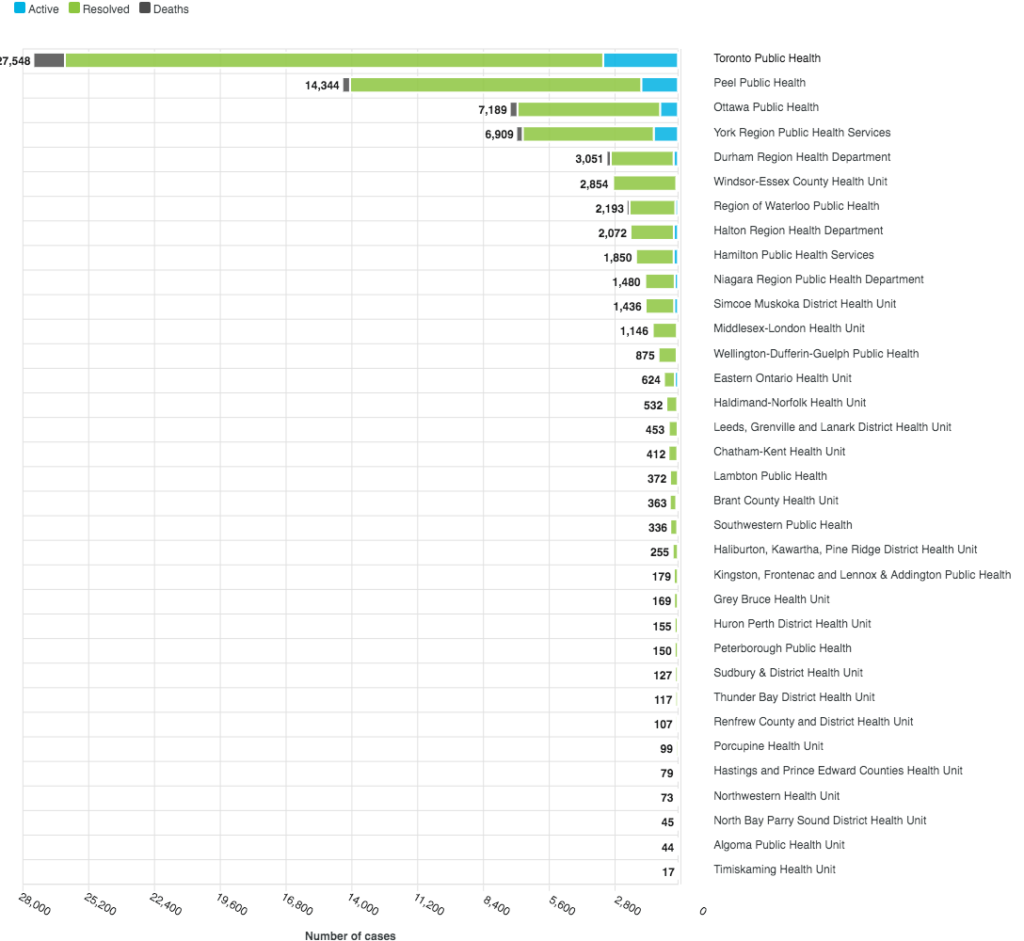

Case statuses

Despite this people figured out how to survive and live amongst a virus that was and is very deadly for a certain group of people.

The chart above illustrates the number of active & resolved coronavirus cases and deaths. Covid-19 is very dangerous for people with compromised health conditions and the elderly as noted above. The majority of deaths occurred between ages 60-99.

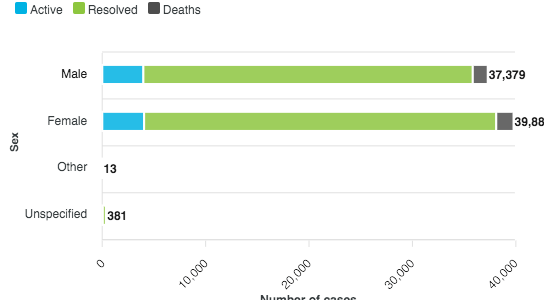

Coronavirus is gender neutral

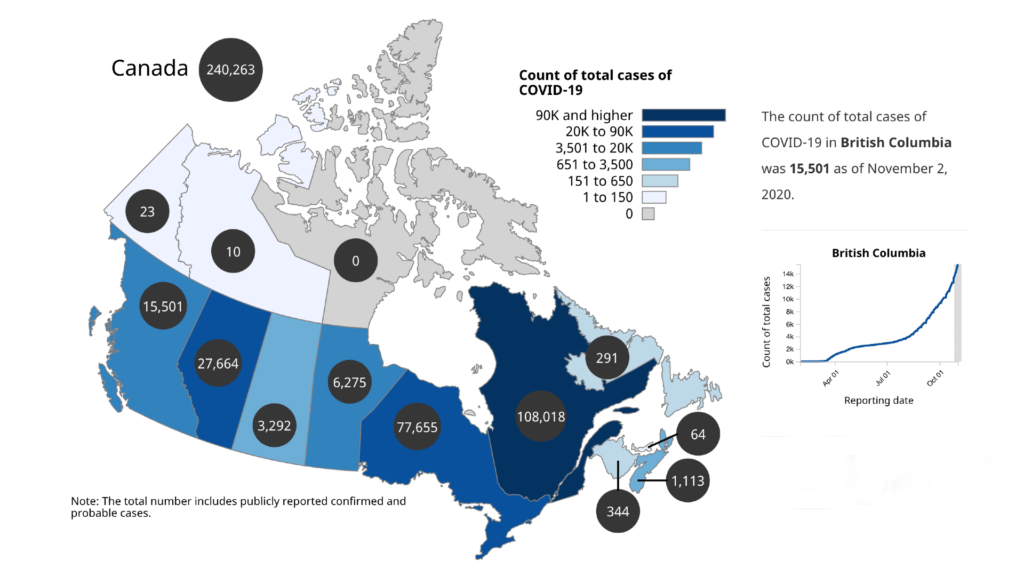

Geographical hot spots

The majority of cases are in Toronto and the Peel region. So what does this mean? There are 14.5 million people in Ontario with 2.9 million residing in Toronto. For a great many people Coronavirus has not been a problem. I don’t want to appear dismissive about this. Coronavirus has killed over 10,000 people in Canada.

The majority of cases (77.3%) and deaths (92.4%) have been reported by Ontario and Quebec.

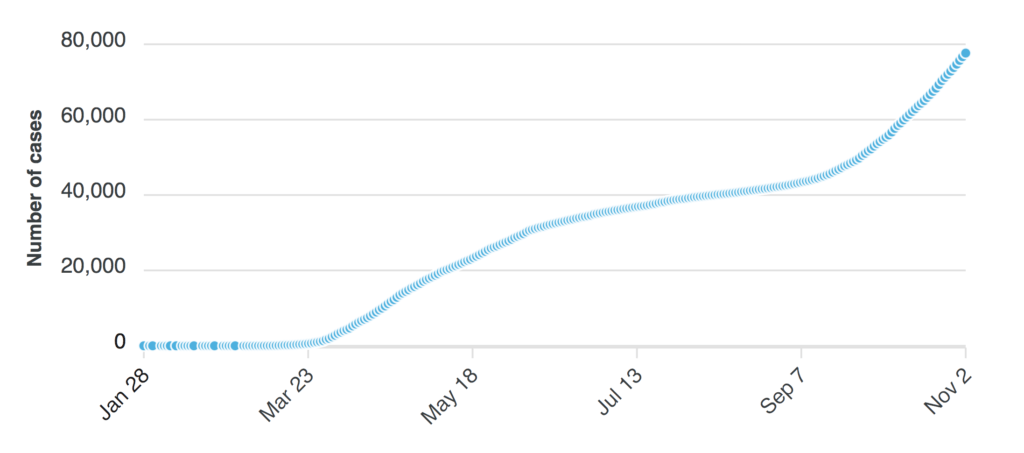

Progression of cases over time

Back to the question of living with the Coronavirus outbreak. While the number of Active cases has gone up dramatically since September the number of deaths has not increased at the same rate. At the beginning of the outbreak, we were extremely unprepared and vulnerable. The province has done an excellent job of educating everyone on how to protect those who are most at risk of contracting the Coronavirus.

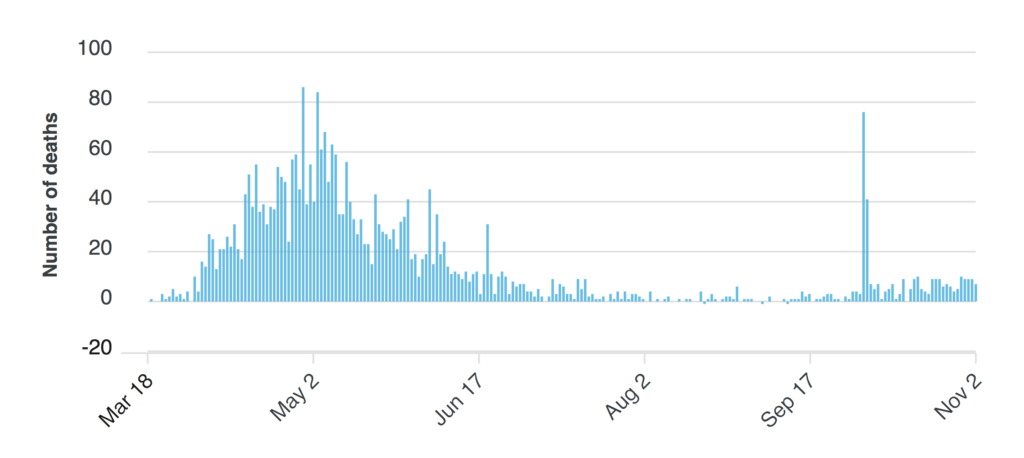

Coronavirus Deaths

Coronavirus New Cases

What is significant about the graphs above, is the contrast between new cases in November being nearly double the new cases at the highest point in April when the province was locked down. At the peak of new daily cases (640) on April 24, there were 50 deaths as compared to October 31 with 1,014 new daily cases and 9 deaths.

What this tells me is we understand how to live with the Coronavirus, how to protect ourselves and the people we love without the province being in lockdown. Everywhere I’ve gone in the GTA people are doing there part to keep safe:

- Wearing a face mask

- Sanitizing their hands, even the items they purchase

- Utilizing hands-free door openers

- Maintaining separation of at least 2 metres

- Avoiding unnecessary travel

- Learning how to work with digital products to conduct business

People have decided they can continue to work and to be social in a safe way. They have the tools, knowledge, and experience to move forward with their life without endangering others, especially those among us who are most vulnerable.